How to Split Money With Your Partner

Key Takeaways

Splitting expenses evenly does not always create fairness when partners earn different incomes. An income-based contribution often creates better balance.

Many couples maintain individual accounts and contribute to a shared account for joint expenses such as housing, groceries, and household costs.

Financial systems should evolve with life changes, including career shifts, caregiving responsibilities, debt, or major financial decisions.

Building a shared life is a meaningful step.

Whether you’re moving in together, getting married, or revisiting how money works years into a relationship, it often comes with excitement, relief, and a quiet question that surfaces sooner or later:

How do we actually handle money now?

Groceries become shared. Utilities are shared. Housing costs are shared. Decisions that once belonged to one person now affect two. And while combining parts of your life can feel natural, combining finances often brings uncertainty, especially when circumstances are not equal.

What if one of you earns more?

What if one of you owns the home?

What if one of you carries more debt, or has less flexibility, or has already made career sacrifices for the relationship?

There is no single “right” way to combine finances. What matters most is that the system you choose feels fair, sustainable, and respectful to both people involved.

For many couples, this becomes one of the most emotionally loaded conversations. And while every relationship is different, there is one approach many couples find helpful when incomes are unequal: contributing to shared expenses based on income, not splitting everything evenly.

Let’s walk through what that looks like, why it works, and how to adapt it to your relationship.

Why “Equal” Does Not Always Mean Fair

Many couples default to splitting expenses 50/50. On the surface, it feels simple and neutral. Each person pays half, and no one owes the other anything.

But when incomes differ meaningfully, a 50/50 split can quietly create imbalance.

One partner may be using most of their paycheck just to cover shared bills, while the other has far more room for saving, spending, or flexibility. Over time, this can show up as resentment, guilt, or a subtle power dynamic around money, even when both partners have good intentions.

Fairness in a partnership is not about equal dollars. It’s about equal impact.

A system that looks neutral on paper can feel heavy in real life, especially if one person consistently feels stretched or financially constrained.

This is where an income-based approach can help restore balance.

A More Grounded Framework: Splitting Expenses Based on Income

Instead of asking each partner to contribute the same dollar amount, this approach asks each partner to contribute the same percentage of their income toward shared expenses.

The goal is not to merge everything or eliminate autonomy. It is to align responsibility with capacity, while preserving independence.

This structure tends to work well for couples who value transparency, autonomy, and mutual respect, especially when incomes are not equal or may change over time.

Step 1: Preserve Individual Accounts and Add One Shared Account

Each partner keeps their own checking account.

Individual accounts preserve:

Autonomy

Privacy

A sense of personal agency

Then, together, you open one joint checking account. This account exists for shared expenses only.

Common shared expenses might include:

Rent or mortgage

Utilities

Internet and streaming services

Groceries and household supplies

Childcare or shared family costs

Joint savings goals

What counts as “shared” is a decision you make together. There is no universal list, and there shouldn’t be.

Step 2: Calculate Income Percentages

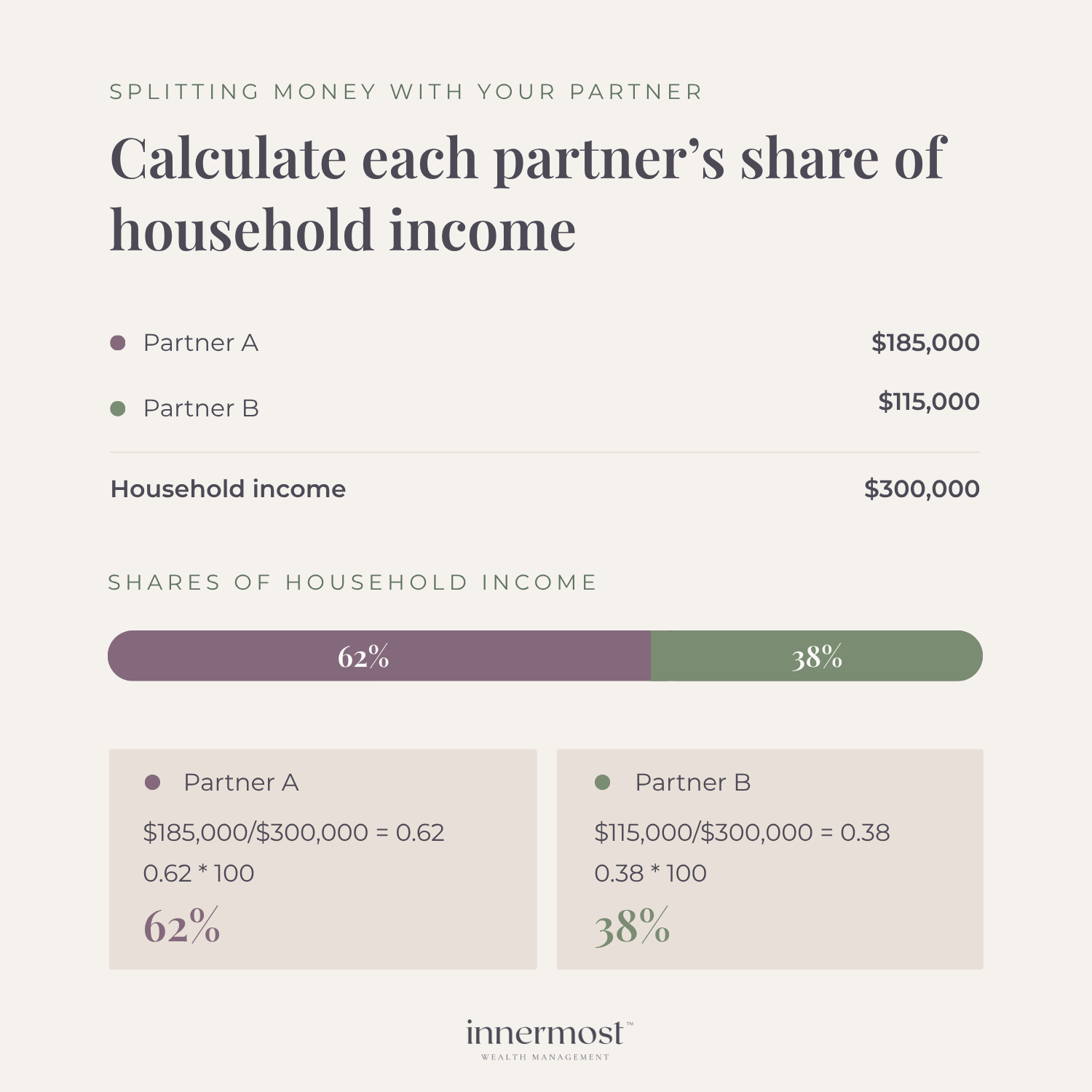

Add up your total household income.

Then calculate what percentage of that total each partner earns.

For illustration:

Partner A earns $185,000

Partner B earns $115,000

Total household income is $300,000

Partner A earns 62% of the household income. Partner B earns 38%.

These percentages become the foundation of your shared expense plan.

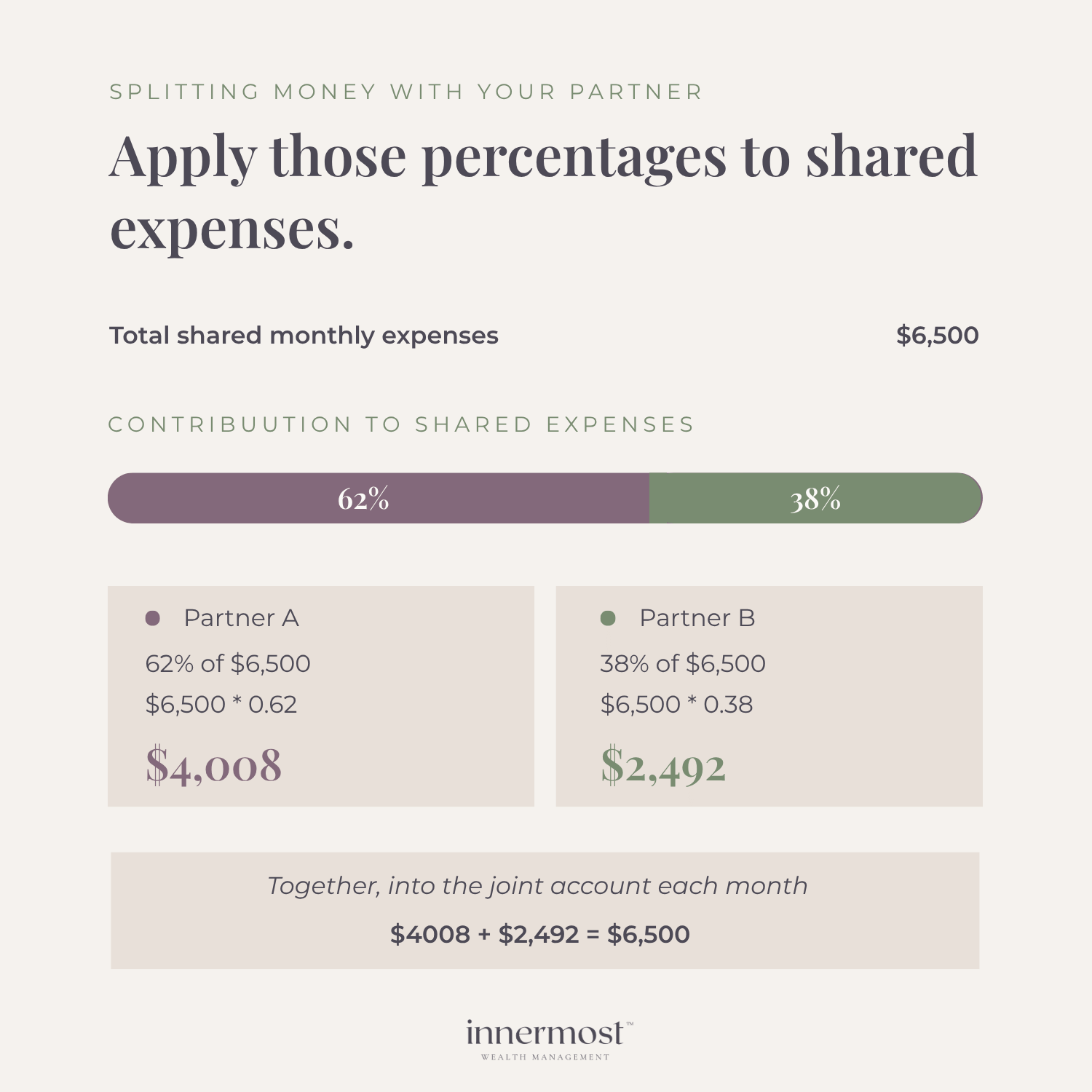

Step 3: Apply Those Percentages to Shared Expenses

Next, add up your shared monthly expenses.

Let’s say they total $6,500 per month.

Partner A contributes 62%, or $4,008. Partner B contributes 38%, or $2,492.

Each partner transfers their share into the joint account monthly, or per paycheck if that feels easier to manage.

Once the money is there, bills are paid from the joint account. What remains in each person’s individual account stays theirs.

This structure can allow both partners to contribute meaningfully without one person carrying a disproportionate burden.

Why This Often Feels More Sustainable Over Time

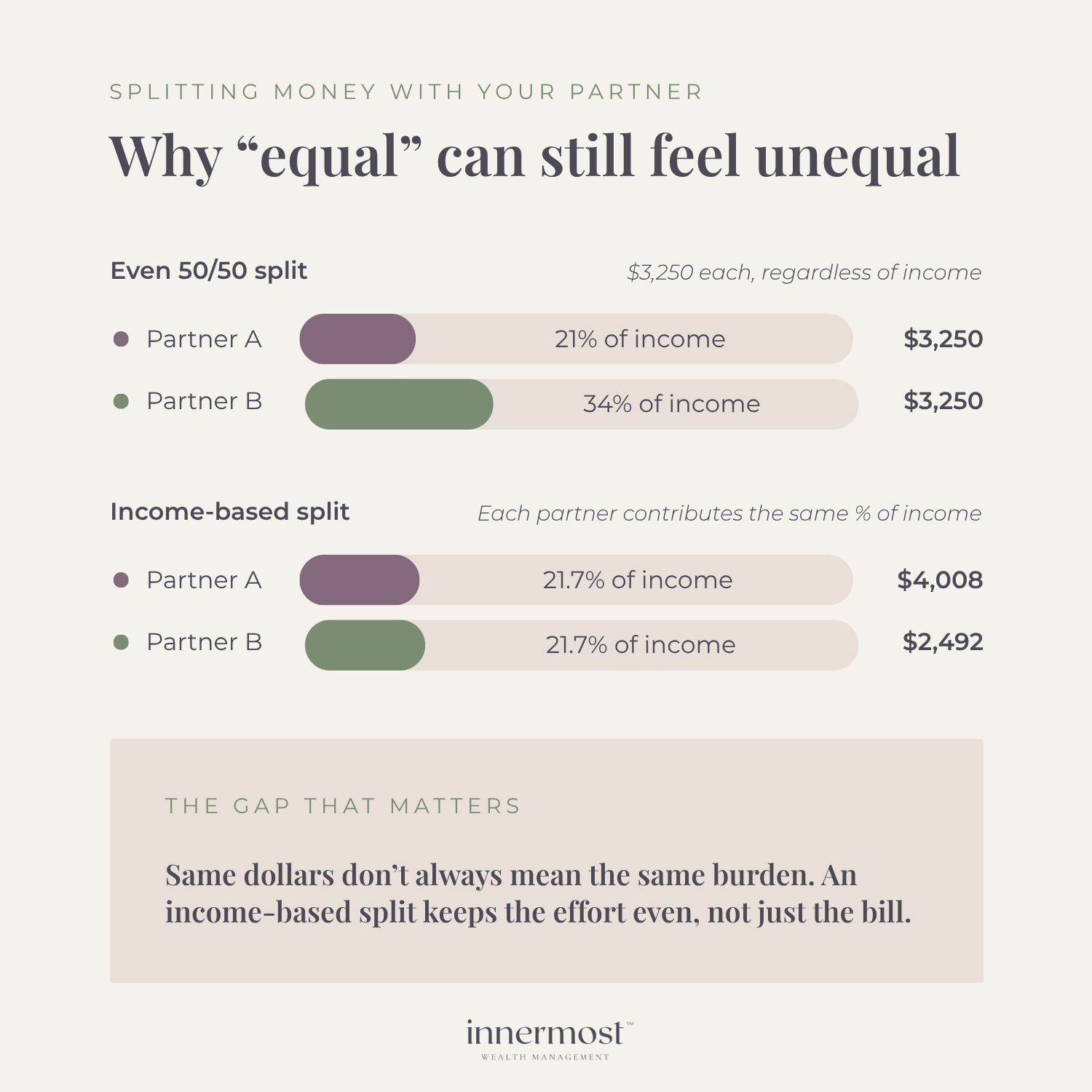

Using the example above, compare this to a 50/50 split.

If each partner paid $3,250 per month:

Partner A would be spending roughly 21% of their income on shared expenses

Partner B would be spending about 34%

That gap matters.

Over time, it influences who feels constrained, who feels comfortable, and who has more choice. It can affect decisions about travel, savings, or even day-to-day spending.

An income-based split recognizes that equal dollar amounts aren't always equal sacrifices. Instead, it aims to distribute shared expenses in a way that feels fair relative to each person's financial situation.

Customizing What Counts as “Shared”

This framework is flexible by design. The most important step is deciding together what belongs in the joint category.

Some couples only share core household costs. Others take a broader view.

For example:

Car payments may stay individual, especially if they reflect personal preferences

Work-related costs might stay individual if only one partner incurs them

If one partner works from home, you may decide they contribute slightly more to utilities

If one partner commutes, transportation costs may be treated as individual

The guiding question is not “Whose expense is this?” but “How do we want to support each other’s financial stability?”

Ownership, Assets, and Unequal Starting Points

Money dynamics become more complex when one partner owns the home, has significant investments, or entered the relationship with more assets.

In these situations, a 50/50 approach can feel especially misaligned.

For example, if one partner owns the home and the other contributes to ongoing expenses, it’s important to clarify:

What payments are considered rent versus shared costs

Whether contributions build equity or not

How long-term fairness is being defined

These conversations are not about keeping score. They are about setting expectations and protecting trust.

Debt and Long-Term Capacity

Debt often carries emotional weight and unspoken assumptions.

In some relationships, each partner keeps their own debt separate. In others, minimum payments are factored into shared planning.

If one partner’s debt consumes most of their remaining income, it can limit shared experiences and long-term goals, even if the debt itself is not shared.

There is no obligation to take on someone else’s debt. But there can be value in acknowledging its impact and planning with it in mind.

When Careers Shift or Sacrifices Are Made

Income-based systems work particularly well when life changes.

If one partner steps back from work, goes back to school, relocates for the relationship, or takes on more caregiving responsibilities, income may shift temporarily or permanently.

A flexible structure allows the financial system to adjust without one person feeling penalized for choices that support the partnership as a whole.

This is where fairness becomes deeply relational, not mathematical.

Transparency

No system works without honesty.

Whatever approach you choose, both partners need a shared understanding of:

Income

Expenses

Obligations

Goals

Avoiding money conversations can feel easier in the short term, but it can create more stress over time. Both partners should feel safe enough to be honest about where they’re at and where they want to go, both individually and as a team. Handling financial transparency with care can actually deepen the trust in a relationship.

Navigating these conversations is a skill. For a closer look at applying these transparency principles to your marriage prep, see our guide: How to Discuss a Prenup Without the Stress.

Revisiting the Plan as Life Evolves

Your financial arrangement does not need to be permanent. This is true whether you’re setting things up for the first time or reworking a system that no longer fits your life today.

Incomes change. Careers evolve. Family structures shift. The system that works today may not work five years from now.

We encourage couples to treat their financial structure as something to revisit periodically, not something they “get right” once.

Checking in allows your plan to grow with you rather than quietly working against one of you.

A Note on Power and Autonomy

Money systems are not just logistical. They shape how power is felt and expressed in a relationship.

When one partner consistently feels stretched while the other feels comfortable, it can affect confidence, safety, and emotional balance.

A thoughtful approach to shared finances is one way couples can reinforce mutual respect and autonomy, even when circumstances are unequal.

Final Thoughts

There is no perfect formula for combining finances with a partner. The goal is not symmetry. It is balance.

An income-based approach to shared expenses is one option that often helps couples navigate differences in earning power without sacrificing independence or fairness.

What matters most is that your system reflects your values, your reality, and the life you are building together.

If you’d like to explore how financial planning conversations like this fit into your broader financial plan, you’re welcome to schedule a conversation here.

Frequently Asked Questions About Splitting Expenses With Your Partner

Below are common questions we address in planning conversations.

-

There is no universal formula, but fairness is rarely the same as splitting everything 50/50.

For couples with unequal incomes, contributing to shared expenses based on income percentage often creates more balance. This approach aligns responsibility with earning capacity, helping both partners contribute meaningfully without one person feeling financially strained.

-

Not necessarily.

Some couples choose to fully combine finances, while others maintain separate accounts and contribute to a shared joint account for household expenses. The right structure depends on your values, communication style, income levels, and long-term goals.

Maintaining individual accounts alongside a joint account often preserves autonomy while still supporting shared responsibilities.

-

When incomes differ meaningfully, a 50/50 split can create imbalance over time.

An income-based approach, where each partner contributes the same percentage of their income toward shared expenses tends to feel more sustainable. This structure adjusts naturally if incomes change and reduces the risk of resentment or financial pressure within the relationship.

-

If one partner owns the property, it’s important to clarify expectations early.

Discussions should address whether contributions are considered rent, shared expenses, or equity-building payments. Clear agreements protect both partners and prevent misunderstandings about ownership and long-term fairness.

These conversations are less about keeping score and more about setting transparent expectations.

-

Financial systems should be revisited after major life changes including promotions, career shifts, relocation, children, business launches, or income changes.

Even without major events, reviewing your system annually ensures it still reflects your goals, earning capacity, and shared priorities.

Money systems should evolve as your relationship evolves.