Life Insurance Planning: How Much Coverage Do You Need?

Key Takeaways

Life insurance planning is a foundational form of financial protection, designed to preserve income, stability, and continuity for the people who depend on you.

Term life insurance is often appropriate for high-earning professionals in their peak earning years, while permanent policies may serve more advanced estate or liquidity planning needs.

The appropriate amount of coverage depends on income replacement needs, outstanding obligations, and long-term financial goals.

Employer-provided life insurance is typically supplemental and may not be sufficient for households with mortgages, children, or business exposure.

Life insurance decisions should be evaluated within the context of a broader financial plan, including estate strategy, tax considerations, and risk management.

There are certain financial conversations that feel productive. Investing. Buying a home. Negotiating compensation.

And then there are the conversations we quietly postpone.

Estate planning. Incapacity. Death.

Life insurance planning sits in that second category for most people. It can feel abstract, uncomfortable, or far away. But for many families, especially those with children, dependents, business ownership, or significant income, it is one of the most foundational forms of protection.

Life insurance is not about fear. It is about responsibility. It is about preserving stability for the people and structures that depend on you.

And in many cases, it is far more nuanced than simply “Do I have kids?”

This guide walks through how life insurance works, who actually needs it, and how to determine the right amount of coverage.

Let’s walk through it together.

What Life Insurance Actually Is

At its core, life insurance is a contract.

You pay premiums to an insurance company. In exchange, if you pass away while the policy is active, the insurer pays a designated amount, known as the death benefit, to your chosen beneficiaries.

That benefit can be used for anything: income replacement, debt repayment, mortgage payoff, education funding, business transition, estate taxes, or simply preserving the lifestyle your family relies on.

The purpose is straightforward: if your income, labor, or financial presence disappeared tomorrow, would the people connected to you be financially secure?

Life insurance is one tool families may use to address that question in advance.

Primary Types of Life Insurance

Understanding structure matters, because not all policies serve the same purpose.

Term Life Insurance

Term insurance covers you for a defined period of time, typically 10, 20, or 30 years.

If you pass away during that period, your beneficiaries receive the benefit. If you outlive the term, the policy expires.

Term policies are often:

More affordable

Straightforward

Designed primarily for income replacement during high-earning or child-rearing years

For many professionals in their 30s and 40s building careers, raising children, and carrying mortgages, term coverage is commonly used to address income replacement needs.

It is protection during the years you are most financially essential.

Whole Life Insurance

Whole life is a type of permanent insurance. It remains in force for your entire lifetime, as long as premiums are paid.

In addition to the death benefit, it includes a cash value component that grows over time on a tax-deferred basis.

This cash value can be accessed through loans and may provide additional planning flexibility.

Whole life policies are typically:

Significantly more expensive than term

Structured with fixed premiums

Used in more complex estate planning or wealth transfer strategies

They are rarely necessary for everyone, but in high-net-worth or advanced planning scenarios, they can serve a purpose.

Universal Life Insurance

Universal life is another form of permanent insurance, but with more flexibility in premiums and internal growth.

Some versions are conservative. Others introduce market exposure.

These policies can be useful in very specific planning contexts, but they require careful review. Assumptions around growth rates and costs matter significantly over time.

As with any financial tool, complexity does not equal superiority. The design must match the need.

Do You Actually Need Life Insurance?

This is where nuance matters.

Life insurance is not mandatory. It is situational.

Here are the circumstances where it deserves serious consideration.

If Someone Depends on Your Income

If you have children, a spouse, aging parents, or any person whose financial stability relies on your earnings, insurance becomes less about you and more about them.

Income replacement is not simply about replacing salary. It may also include:

Funding childcare

Covering household management

Maintaining health insurance

Paying for education

Preserving housing stability

If your absence would create immediate financial disruption, life insurance is a responsible form of continuity planning.

If You Carry Debt with Shared Exposure

Some debts do not disappear when you do.

Private student loans often do not discharge upon death. Loans with cosigners transfer responsibility. Mortgages tied to joint ownership may leave one party financially strained.

If someone else would be financially burdened by your obligations, insurance can neutralize that risk.

Federal student loans are typically discharged upon death. Private loans are not guaranteed to be.

This is not widely understood, and it matters.

If You Are a Business Owner

Business ownership introduces additional layers.

What happens to the business if you pass unexpectedly?

Are there partners? Employees? Clients? Active contracts?

In many cases, life insurance funds:

Buy-sell agreements

Ownership transitions

Payroll continuity

Operational stability during restructuring

Without a plan, the business may become vulnerable precisely when stability is most needed.

If You Have a Significant Estate

For higher-net-worth families, life insurance can serve a strategic multi-generational estate planning function.

It may:

Offset estate tax exposure

Equalize inheritances

Provide liquidity to heirs

Preserve assets such as real estate or family businesses

In this context, life insurance is less about income replacement and more about tax and transfer efficiency. Please note that insurance strategies should be evaluated in coordination with a qualified tax professional and estate planning attorney.

If You Have Minimal Savings

Funeral and burial expenses in the United States often range between $7,000 and $15,000 depending on services and location. That does not include medical expenses, probate costs, or outstanding obligations.

If your savings would not cover these expenses, the financial burden may fall on family members.

Life insurance ensures that grief is not compounded by immediate financial stress.

Health, Timing, and Insurability

Life insurance underwriting typically includes a medical evaluation. Insurers assess:

Height and weight

Blood pressure

Cholesterol levels

Medical history

Family history

Smoking status

Premiums are directly influenced by health profile at the time of application.

As a result, timing can influence underwriting outcomes.

If you are planning a pregnancy, it is often advantageous to secure coverage before becoming pregnant or after recovery. Temporary physiological changes can impact underwriting metrics.

If you have a family history of serious illness, earlier coverage may offer more favorable premiums and broader approval options.

Waiting until a diagnosis can significantly increase costs or limit eligibility.

This is one of the few areas in financial planning where proactive action has outsized impact.

How Much Life Insurance Do You Need?

There is no universal formula. Coverage should reflect your obligations, your goals, and the life you are supporting.

That said, there are three primary frameworks we use to think about the decision.

Income Replacement

Some planning approaches begin by estimating income replacement needs over a period of years.

This method answers a straightforward question: if your income disappeared tomorrow, how long would your household need meaningful financial stability?

For many high-earning professionals, especially those supporting children or carrying significant fixed costs, lower multiples often underestimate the true impact of income loss.

Still, income multiples are only a starting point. They rarely account for inflation, education funding, or long-term wealth-building goals. More precise planning often requires deeper modeling.

Capital Needs Analysis

This approach is more deliberate.

Instead of relying on a multiple, you calculate the actual financial obligations that would remain:

Remaining mortgage balance

Outstanding debts

Future education funding

Funeral and final expenses

Desired income replacement period

The value of unpaid contributions such as childcare or household management

From that total, you subtract:

Existing savings and investments

Employer-provided life insurance

Other available assets

The difference becomes the coverage gap.

For high-earning dual-income households, business owners, or families with complex balance sheets, this method often provides greater clarity than a simple income multiplier.

Human Life Value

This is the most analytical approach.

It calculates the present value of your future earnings through retirement, adjusted for taxes and personal consumption.

Most households do not require this level of modeling. But in advanced planning scenarios, particularly for business owners or families with substantial income concentration, it can be useful.

At Innermost Wealth Management, we help clients evaluate protection decisions like life insurance within the context of their broader financial plan to align with responsibilities, long-term goals, and evolving life circumstances. Schedule a conversation here if you would like to review how protection strategies like life insurance fit within your broader financial plan.

Employer Coverage: Is It Enough?

Many employers provide life insurance, often 1–2 times salary.

This is helpful, but rarely sufficient for households with mortgages, children, or long-term obligations.

It also:

Is tied to employment

May not be portable

May not follow you if you change jobs

Employer coverage should be viewed as a supplement, not a complete solution.

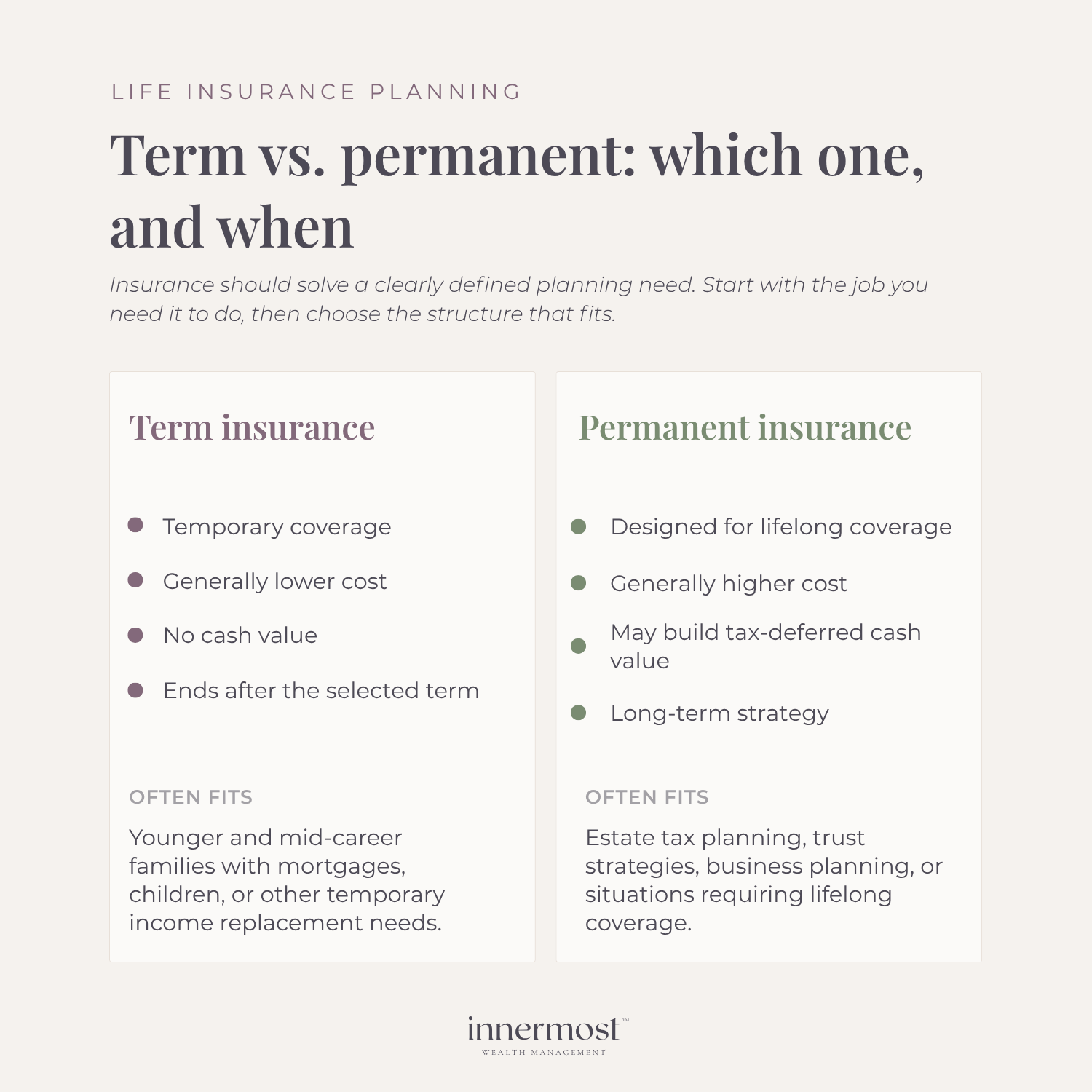

Term vs Permanent: A Grounded Perspective

For most young to mid-career professionals building wealth, term insurance is typically appropriate. It is designed to cover the years when income replacement matters most and financial obligations are highest.

Permanent policies may make sense in more specific circumstances, such as:

Estate tax exposure

Advanced trust or liquidity planning

Situations requiring lifelong coverage

Insurance should solve a clearly defined planning need. It should not be positioned as an investment substitute without thoughtful analysis.

Some permanent policies are structured in ways that make them expensive to unwind later. Before committing to any long-term insurance contract, it is important to understand the costs, flexibility, and long-term implications.

The Emotional Side of the Decision

There is a psychological component here.

Thinking about mortality is uncomfortable. Many avoid it entirely.

But planning for the unlikely is an act of stability. It signals to your family: if something happens, the financial foundation holds.

It can help reduce uncertainty.

In many ways, life insurance is not about death. It is about reducing anxiety while you are alive.

How This Fits Into Your Broader Plan

Life insurance does not stand alone. For many families, life insurance decisions also intersect with how assets are ultimately passed down and received. If you’re navigating what happens after wealth is transferred, this guide on what to do with an inheritance walks through the financial and emotional decisions that come next.

It intersects with:

Estate planning

Beneficiary designations

Disability insurance

Business continuity planning

The goal is not simply to “have a policy.” It is to ensure that your overall financial structure can withstand disruption.

Please note, Innermost Wealth Management, LLC is a fee-only registered investment adviser and does not sell insurance products or receive commissions from insurance policies.

Final Thoughts

Life insurance is rarely urgent. It is rarely exciting.

But it is foundational.

If someone relies on you financially, if your absence would create instability, or if your estate structure carries complexity, it deserves thoughtful consideration.

This is not about fear-based planning. It is about protecting continuity.

When aligned properly, life insurance allows your family, your business, and your long-term intentions to remain intact, even if you are not there to guide them.

And that is ultimately what financial planning is designed to do: preserve stability, clarity, and choice across all seasons of life.

If reviewing your coverage feels overdue, this is the kind of planning conversation we walk through with clients regularly. You can schedule a conversation here.

Frequently Asked Questions About Life Insurance

Below are frequently asked questions we address in planning conversations.

-

Many households with income replacement needs consider term insurance during their working years.

Permanent insurance may be appropriate for estate planning, liquidity needs, or advanced wealth transfer strategies. The right answer depends on whether the need is temporary or lifelong.

-

Employer coverage is helpful but often limited to one or two times salary. For families with mortgages, children, or long-term financial obligations, that amount may not fully protect dependents. Employer policies are also tied to your job and may not be portable.

-

Some insurers offer simplified or no-exam policies, but premiums are typically higher and coverage amounts may be lower. For healthy applicants, traditional underwriting often results in more competitive pricing.