Retirement Planning: Why Retirement Isn’t About Stopping Work — It’s About Choice

Key Takeaways

Modern retirement planning is less about reaching a specific age and more about creating the financial independence to choose how you spend your time.

Financial independence allows work to become optional, giving you flexibility to pursue meaningful work, family priorities, or personal interests without financial pressure.

A thoughtful retirement strategy integrates investments, tax planning, insurance, and lifestyle planning to support both financial security and emotional wellbeing.

When people think about retirement, they often imagine it as a finish line. One day you’re working, the next you’re not.

But for many professionals today, that definition doesn’t quite fit.

Retirement isn’t about abruptly stopping work. It’s about having the freedom to decide how, when, and if you want to work.

At Innermost Wealth Management, we often see clients reach a point where their perspective shifts. Instead of asking, “When can I retire?” the question becomes:

“When will I have the flexibility to choose how I spend my time?”

That shift is subtle, but powerful.

True retirement planning is really about building the financial independence that allows you to design your life intentionally. For some people that means leaving a demanding career earlier than expected. For others, it means continuing to work in a way that feels meaningful without the pressure of needing the income.

Either way, the common thread is choice.

What Is Retirement Planning?

Retirement planning is the process of building financial security so you can support your lifestyle without relying entirely on employment income.

A thoughtful retirement planning strategy typically includes investment strategy, tax planning, savings accumulation, risk management, and long-term income planning.

For many professionals today, retirement planning is less about choosing a specific retirement age and more about creating the financial independence to make work optional.

This may involve:

Maximizing employer retirement plans

investing in brokerage accountsManaging tax-efficient withdrawals later in life

Planning for healthcare costs and longevity

A well-designed retirement strategy aligns your financial resources with the kind of life you want to live.

Redefining Retirement in Today’s World

The traditional retirement model was built for a different era.

For decades, many workers followed a predictable path: work for the same company for most of your career, retire around age 65, and rely on a pension and Social Security for income. While the landscape has changed, understanding how to optimize your Social Security benefits remains a cornerstone of a reliable income strategy.

That structure shaped how people thought about retirement planning.

But the reality today looks very different.

Careers are more dynamic. People change jobs, start businesses, take sabbaticals, or pivot into new industries later in life. Life expectancy has increased significantly. And fewer workers rely on pensions as a primary source of retirement income.

As a result, retirement has become less of a fixed milestone and more of a transition.

For many of the women and families we work with, the goal is not necessarily to stop working altogether. The goal is to remove financial pressure so that work becomes optional rather than necessary.

That difference changes everything.

When financial independence becomes the focus, retirement planning stops being about a date on the calendar and starts becoming about designing a life that feels aligned with your priorities.

Financial Independence as the Goal

At its core, retirement planning is really about financial independence.

Financial independence means that your savings and investments can sustainably support your lifestyle without relying entirely on employment income.

When that foundation exists, your relationship with work changes.

Instead of needing to work to maintain your lifestyle, you can choose to work because it feels meaningful, interesting, or fulfilling.

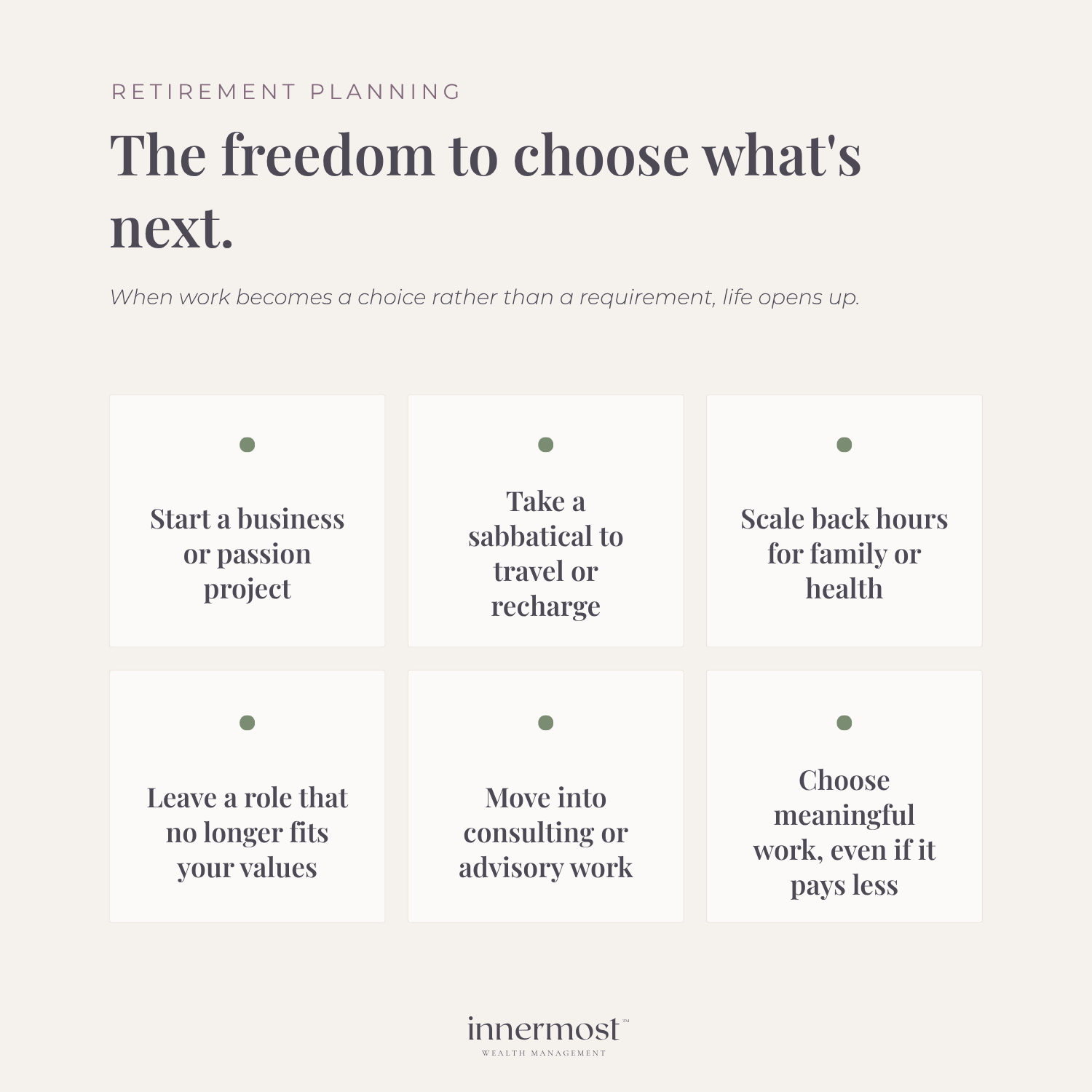

Financial independence can create opportunities such as:

Leaving a job that no longer aligns with your values or wellbeing

Scaling back hours to prioritize family or personal health

Taking a sabbatical to travel or pursue a personal project

Starting a business or passion project later in life

Transitioning into consulting or advisory roles

Pursuing work that feels meaningful even if it pays less

The common thread across all of these scenarios is flexibility.

And flexibility is one of the most valuable forms of wealth.

What “Work Optional” Really Means

You may hear the phrase “work optional” used in financial planning conversations.

A work-optional lifestyle means you have the financial security to cover your living expenses through savings, investments, and other income sources. Work becomes something you can choose rather than something you must do.

For high-earning professionals in particular, this mindset can be incredibly empowering.

Many people reach a point in their careers where the question isn’t simply about retiring early. It’s about having the freedom to step away from environments that no longer feel aligned.

Sometimes that means leaving a demanding role.

Sometimes it means negotiating greater flexibility.

Sometimes it means reinventing your career entirely.

But those decisions are far easier to make when your financial foundation supports them.

A thoughtful retirement strategy is what makes that possible. In this retirement planning case study, we walk through how one family approached the transition from full-time work to financial independence with a clear plan.

Key Components of a Thoughtful Retirement Plan

While every person’s financial situation is unique, most retirement plans are built around a few core elements.

Understanding your lifestyle needs

The first step in retirement planning is understanding what kind of life you want to support.

How much do you spend today?

What expenses might change in the future?

Some costs may decrease over time, such as commuting or childcare. Others may increase, including travel, healthcare, or supporting family members.

A clear understanding of your lifestyle needs provides the foundation for calculating how much financial independence actually requires.

Building wealth intentionally

Once lifestyle needs are understood, the next step is building an investment strategy designed to support long-term financial independence.

For many professionals, this includes a combination of:

Employer retirement plans such as 401(k)s

Individual retirement accounts (IRAs or Roth IRAs)

Brokerage investment accounts

Equity compensation such as RSUs or stock options

Health savings accounts (HSAs)

Business ownership or real estate investments

Each account type has different tax characteristics and planning opportunities.

Coordinating them thoughtfully can significantly increase long-term flexibility and tax efficiency.

Managing taxes over time

Tax strategy plays an important role in retirement planning.

Decisions about when to contribute to tax-deferred accounts, when to use Roth strategies, and how to manage withdrawals later in life can have a significant impact on the longevity of your portfolio.

Thoughtful tax planning can help reduce unnecessary tax drag and preserve more of your wealth for future use.

Protecting your financial foundation

A strong retirement plan also includes risk management.

Insurance coverage, estate planning documents, and asset protection strategies help ensure that unexpected events do not derail your long-term financial independence.

For many families, this includes coordinating:

Disability insurance

Estate planning documents such as wills and trusts

Healthcare directives and powers of attorney

These protective layers may not feel exciting, but they are essential to maintaining stability.

Building flexibility into the plan

One of the most important aspects of retirement planning is flexibility.

Life rarely unfolds exactly as expected.

Career opportunities arise. Family needs change. Health circumstances evolve.

A thoughtful plan allows for adjustments over time rather than assuming a single rigid path.

Flexibility creates resilience, which is one of the most valuable outcomes of long-term financial planning.

The Psychology of Retirement Planning

Retirement planning isn’t only about numbers.

It also involves an emotional and psychological transition.

Work often provides more than just income. It can also provide identity, structure, and community.

Stepping away from that structure can bring mixed emotions. For some people, the transition brings excitement and freedom. For others, it can trigger uncertainty about purpose, identity, or security.

This is especially true for professionals who have spent decades building their careers.

That’s why thoughtful retirement planning includes both financial preparation and emotional preparation.

When clients approach retirement with intention, they often begin exploring questions such as:

What activities bring me a sense of meaning or contribution?

How do I want to spend my time when work becomes optional?

What relationships and communities will remain central in my life?

These questions help ensure that retirement feels like a transition toward something meaningful rather than simply an exit from work.

Financial stress and emotional wellbeing are closely connected. We explore this relationship further in our article on how financial stress impacts mental health.

Why Retirement Planning Is Especially Important for Women

Women face unique financial considerations when planning for retirement.

On average, women live longer than men. They are also more likely to experience career interruptions related to caregiving responsibilities.

In many families, women eventually become the primary financial decision-maker later in life.

Because of these factors, retirement planning for women often requires additional attention to longevity risk, healthcare planning, and financial independence.

Ensuring that women are deeply involved in financial decision-making early in the planning process can help create greater confidence and long-term security.

At Innermost Wealth Management, supporting women in developing that financial confidence is a central part of our work.

Building a Retirement Strategy That Supports Your Life

Ultimately, retirement planning should support the life you want to live.

For some people, that means retiring early.

For others, it means continuing to work in a flexible way that feels fulfilling.

The goal isn’t simply to reach retirement.

The goal is to create the freedom to choose.

A thoughtful retirement strategy works best when it’s part of a broader comprehensive financial planning strategy that coordinates investments, taxes, and long-term goals, so that your future feels both financially secure and personally meaningful.

When those elements come together, retirement stops feeling like an endpoint.

It becomes a transition into a new phase of life designed around what matters most to you.

Final Thoughts

Retirement isn’t just about when you stop working.

It’s about building the financial independence that allows you to decide how you want to spend your time.

With the right planning in place, work becomes optional rather than necessary.

At Innermost Wealth Management, we guide clients through this process with both technical expertise and a thoughtful understanding of the emotional side of financial decision-making.

Frequently Asked Questions About Retirement Planning

Below are common questions we address in planning conversations.

-

Financial independence means having sufficient savings and investment income to support your lifestyle without relying entirely on employment income. When financial independence is achieved, work becomes optional rather than financially necessary.

-

The amount required varies depending on lifestyle, spending patterns, life expectancy, and investment strategy. Many financial planners use projections and withdrawal strategies to estimate how much wealth is needed to support long-term financial independence.

-

A work-optional lifestyle means you have the financial flexibility to continue working if you choose, but you no longer need employment income to maintain your lifestyle. This approach to retirement planning focuses on flexibility and personal fulfillment rather than a specific retirement age.

-

The earlier you begin retirement planning, the more flexibility compound growth can provide. However, thoughtful planning can add value at any stage of life by helping align investments, tax strategies, and long-term goals.

-

Most financial plans should be reviewed annually or whenever major life changes occur. Career changes, family transitions, tax law updates, or market shifts can all affect long-term retirement strategy.