When Should You Take Social Security? What Actually Drives the Right Decision

Key Takeaways

There isn't one "best" age to claim Social Security. The right decision depends on your finances, your priorities, and what gives you the greatest confidence and flexibility in retirement.

Claiming early (as early as age 62) can reduce your monthly benefit but may reduce pressure on your investment portfolio.

Delaying benefits (up to age 70) can increase monthly income and may provide longevity protection.

The most effective Social Security strategy considers your investments, taxes, and long-term retirement goals together.

Most people know they have a choice about when to claim Social Security benefits. You can begin as early as age 62, wait until your full retirement age, or delay until age 70.

The question is which option makes the most sense for you.

That decision can influence your retirement income, taxes, investment withdrawals, survivor benefits, and the role Social Security plays within your overall financial plan.

Common questions include:

Should I claim Social Security at 62, full retirement age, or 70?

Will I receive more money if I wait?

What if I retire before I want to claim benefits?

How does Social Security affect my taxes?

Does claiming early reduce benefits permanently?

How does my decision affect my spouse?

There isn't a single answer that works for everyone. The right claiming strategy depends on your health, other sources of retirement income, tax situation, life expectancy, and personal goals.

In this article, we'll explain how Social Security benefits work, compare the advantages and tradeoffs of claiming at different ages, discuss the tax implications, and review the factors that can help you make a more informed decision.

The Role of Social Security in Retirement

For most retirees, Social Security is intended to provide a foundation of retirement income rather than replace a paycheck entirely. It was designed to supplement personal savings, pensions, and other retirement assets.

One reason Social Security plays such an important role is that it provides features that are difficult to replicate elsewhere. Under current law, benefits generally continue for life, are adjusted annually for inflation through cost-of-living adjustments (COLAs), and aren't tied to day-to-day market performance.

That combination can provide a level of stability that complements other retirement assets. While investment portfolios fluctuate in value and retirement account balances change over time, Social Security continues to provide a predictable source of income each month.

For many retirees, having a reliable income base can make it easier to manage the rest of their retirement plan. It may reduce the need to sell investments during market downturns, provide greater flexibility when deciding where retirement income comes from, and support a more sustainable long-term withdrawal strategy.

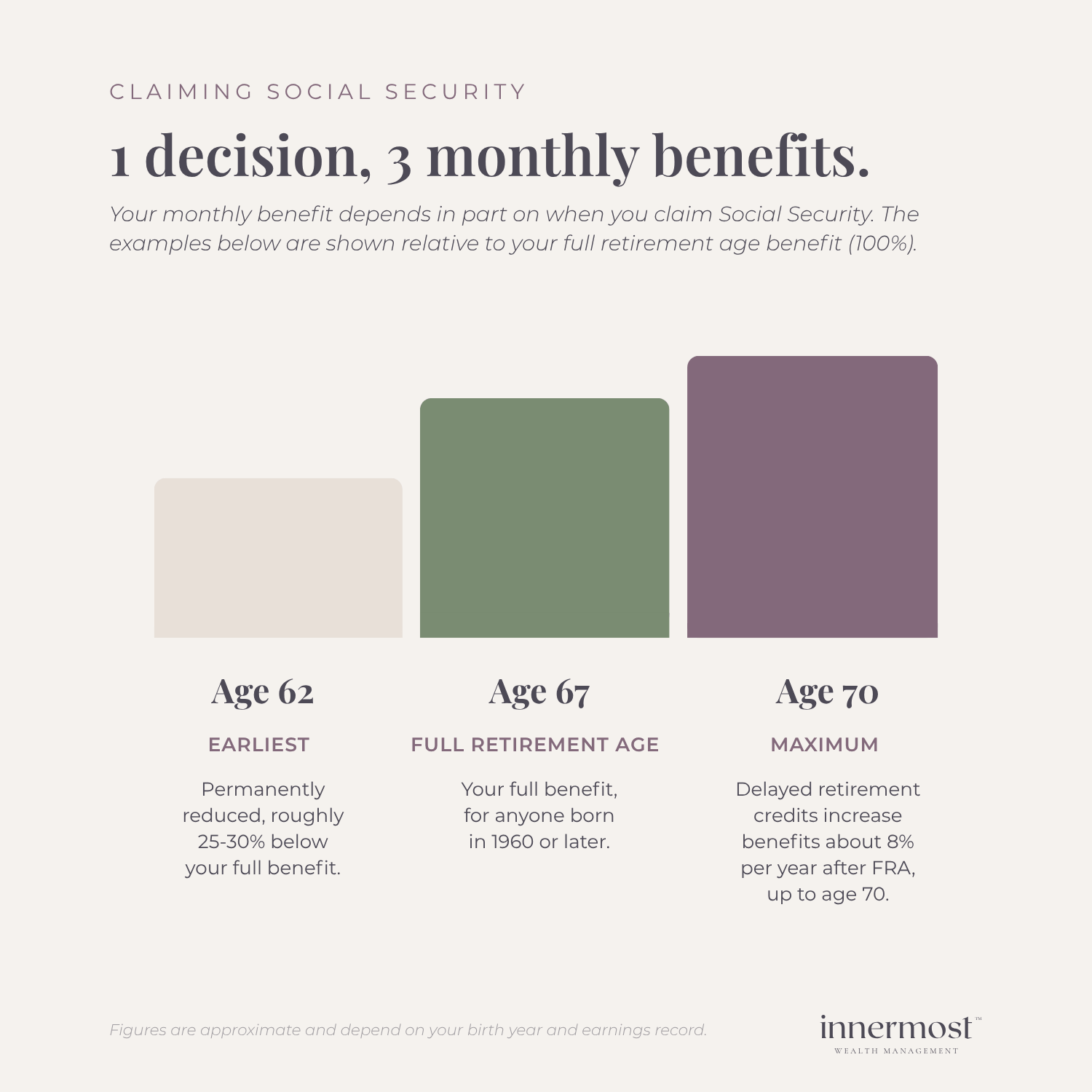

Age 62, Full Retirement Age, or 70: How Claiming Age Affects Your Benefit

One of the biggest Social Security decisions is choosing when to begin receiving benefits. For most people, you can claim as early as age 62, at your full retirement age (FRA), or delay benefits until age 70. The age you choose affects the monthly benefit you'll receive for the rest of your life.

Age 62: The earliest claiming age

You can begin receiving Social Security benefits as early as age 62. However, claiming before your full retirement age results in a permanently reduced monthly benefit. For many people, the reduction is approximately 25% to 30% compared with waiting until full retirement age.

Full retirement age (FRA)

Full retirement age is the age at which you're eligible to receive 100% of your primary insurance amount based on your earnings record. For anyone born in 1960 or later, full retirement age is 67.

Age 70: The maximum benefit

If you delay claiming beyond your full retirement age, your benefit generally increases by about 8% per year until age 70 through delayed retirement credits. After age 70, there is no additional benefit for waiting longer to claim.

For someone with a full retirement age of 67, claiming at age 70 instead of age 62 can result in a monthly benefit that's roughly 75% to 80% higher. The exact difference depends on your birth year and claiming age. Whether delaying results in greater lifetime benefits depends largely on how long you live and your individual circumstances.

Social Security Is Only One Part of Your Retirement Income Plan

Comparing your monthly benefit at age 62, full retirement age, and age 70 is an important part of the decision, but it isn't the only consideration.

When you claim Social Security can influence how much you withdraw from your retirement accounts, how long your investment portfolio may need to support your spending, your overall tax picture, and, for married couples, the income available to a surviving spouse.

That's why the decision isn't simply about collecting the largest monthly benefit or claiming as early as possible. The right strategy depends on how Social Security fits alongside your other retirement income sources, your long-term personal and financial goals, and outlook on the future.

When Claiming Social Security Early May Make Sense

Claiming Social Security before full retirement age isn't always the wrong decision. Depending on your financial situation, health, and retirement goals, it may be the better choice.

1. You retire before full retirement age

If you retire before claiming Social Security, your investment portfolio may need to provide more of your income during the early years of retirement. Starting Social Security earlier can reduce the amount you need to withdraw from your investments, which may help preserve your portfolio during periods of market volatility.

2. Your health or life expectancy is a consideration

If you have health concerns or a family history that suggests a shorter life expectancy, claiming benefits earlier may result in receiving more lifetime income than delaying. While no one knows exactly how long they'll live, health is one of several important factors to consider when evaluating your options.

3. Your retirement spending is higher in the early years

Many people expect their spending to decline once they retire. In reality, the first several years of retirement are often the most active. Travel, hobbies, home improvements, and time with family frequently happen during this period. For some retirees, receiving Social Security sooner may better support those goals than waiting for a larger monthly benefit later.

When Delaying Social Security May Make Sense

Delaying Social Security can be beneficial in a number of situations, particularly for people who expect a long retirement or want a larger source of guaranteed income later in life.

1. You expect a long retirement

Social Security is one of the few sources of retirement income designed to last for the rest of your life under current law. The longer you live, the more valuable a larger monthly benefit can become.

This is especially important for women, who tend to live longer than men on average. Planning for a retirement that could last 30 years or more often means balancing today's income needs with the possibility of needing reliable income much later in life.

2. You want a larger source of predictable income later in retirement

One advantage of delaying Social Security is increasing the amount of predictable monthly income available later in retirement. For some retirees, that can provide greater flexibility when deciding how much to withdraw from their investment portfolio each year, particularly during periods of market volatility.

3. You're married

For married couples, Social Security claiming decisions often affect both spouses. In many cases, the surviving spouse receives the higher of the two Social Security benefits after the first spouse dies. As a result, delaying benefits may increase not only your own retirement income but also the survivor benefit your spouse could receive in the future.

Does Michigan Tax Social Security Benefits?

For Michigan retirees, Social Security benefits aren't subject to Michigan income tax. At the federal level, however, a portion of your Social Security benefits may be taxable depending on your overall income.

Traditional IRA and 401(k) withdrawals, pension income, investment income, capital gains, and other sources of taxable income can all affect how much of your Social Security benefits become subject to federal income tax.

That's one reason Social Security claiming decisions are often evaluated alongside retirement account withdrawals, Roth conversions, and other sources of retirement income rather than on their own.

If you'd like to learn more about how Social Security, retirement account withdrawals, and other income sources work together, you can read my article on Michigan retirement taxes and retirement income planning.

Working While Receiving Social Security

You can continue working while receiving Social Security benefits, but the rules depend on your age.

If you claim Social Security before reaching your full retirement age, your benefits may be temporarily reduced if your earned income exceeds the annual earnings limit established by the Social Security Administration. For 2026, that limit is $24,480. If your earnings exceed the limit, the Social Security Administration generally withholds $1 in benefits for every $2 you earn above the threshold.

In the year you reach your full retirement age, a higher earnings limit applies before benefits are reduced. For 2026, that limit is $65,160, and the reduction is generally $1 for every $3 earned above the limit before the month you reach full retirement age.

Once you reach your full retirement age, there is no earnings limit and your benefits are no longer reduced because of work.

It's also important to understand that these reductions aren't permanently lost. After you reach your full retirement age, the Social Security Administration recalculates your benefit to account for benefits that were previously withheld.

These rules apply to earned income, such as wages or self-employment income. Retirement account withdrawals, pensions, investment income, dividends, capital gains, and similar income sources do not count toward the earnings limit.

Final Thoughts

Choosing when to claim Social Security is one of the most important retirement decisions you'll make because it can affect your income for the rest of your life.

While monthly benefit amounts are important, they're only one part of the decision. Your health, life expectancy, taxes, retirement savings, investment portfolio, marital status, and long-term financial goals all deserve consideration. The best claiming strategy is the one that fits your overall retirement plan.

If you're approaching retirement and would like help evaluating when to claim Social Security as part of a broader retirement income strategy, I'd be happy to help. You can schedule an initial consultation here.

Frequently Asked Questions About When to Take Social Security

-

The appropriate timing depends on factors such as health, life expectancy, financial situation, income needs, and overall retirement planning strategy.

-

Claiming at 62 provides earlier income at a reduced amount. Delaying benefits until age 70 results in higher monthly payments. The appropriate choice depends on your individual circumstances.

-

Social Security retirement benefits increase by approximately 8% per year for each year you delay claiming after full retirement age, up to age 70. This increase is due to delayed retirement credits.

-

Social Security benefits may be taxable depending on your total income. Federal taxation is based on combined income thresholds, and some states also tax benefits. The impact varies based on individual financial circumstances.

-

Yes, you can work while collecting Social Security benefits. If you claim before full retirement age, benefits may be temporarily reduced if your earnings exceed certain limits. After reaching full retirement age, there are no earnings limits.

Sources & Notes

Social Security Administration (SSA.gov) — Retirement Benefits & Claiming Rules

SSA — “How Work Affects Your Benefits” (2026 earnings limits)

IRS — Additional Standard Deduction for Age 65+ (2025–2028 provisions)

Bipartisan Policy Center — Social Security Taxation and Planning Considerations

Tax Foundation — Summary of 2025–2028 Tax Law Changes for Seniors

Social Security rules and benefits are subject to change, and individual outcomes will vary. Please consult with a qualified tax professional regarding your specific situation.