When Ego Enters the Portfolio: What Behavioral Finance Reveals About Confidence and Bias in Investing

Key Takeaways

Investment decisions are influenced not only by markets and data, but also by the psychology of the people making those decisions.

Behavioral finance research shows that biases such as overconfidence and self-attribution can influence how investors interpret success, manage risk, and make future decisions.

Confidence is necessary in investing, but excessive confidence can lead to concentrated bets, excessive trading, and weaker long-term outcomes.

In financial leadership, disciplined processes and intellectual humility often lead to more stable decision-making than bold predictions or personal conviction alone.

Thoughtful financial planning recognizes that money decisions are rarely purely analytical. They are shaped by emotions, experiences, and life transitions.

Finance likes to present itself as purely rational.

Models. Forecasts. Risk metrics.

But anyone who has worked inside the industry eventually notices something else shaping decisions.

Personality.

In environments where decisions involve large sums of capital, public reputation, and asymmetric power, psychology becomes part of the investment process itself.

And occasionally, something more specific enters the portfolio.

Ego.

A manager who believes their instincts are better than the market.

An investor convinced they have identified an opportunity others are missing.

A portfolio strategy that becomes harder to question as early successes accumulate.

In those moments, the portfolio may no longer be shaped only by analysis.

Behavioral finance research suggests this happens more often than many people realize. And when it does, the consequences can influence everything from trading behavior to long-term investment outcomes.

Understanding how confidence and bias shape financial decision-making offers an important lens into how investment leadership actually works.

What the Research Shows

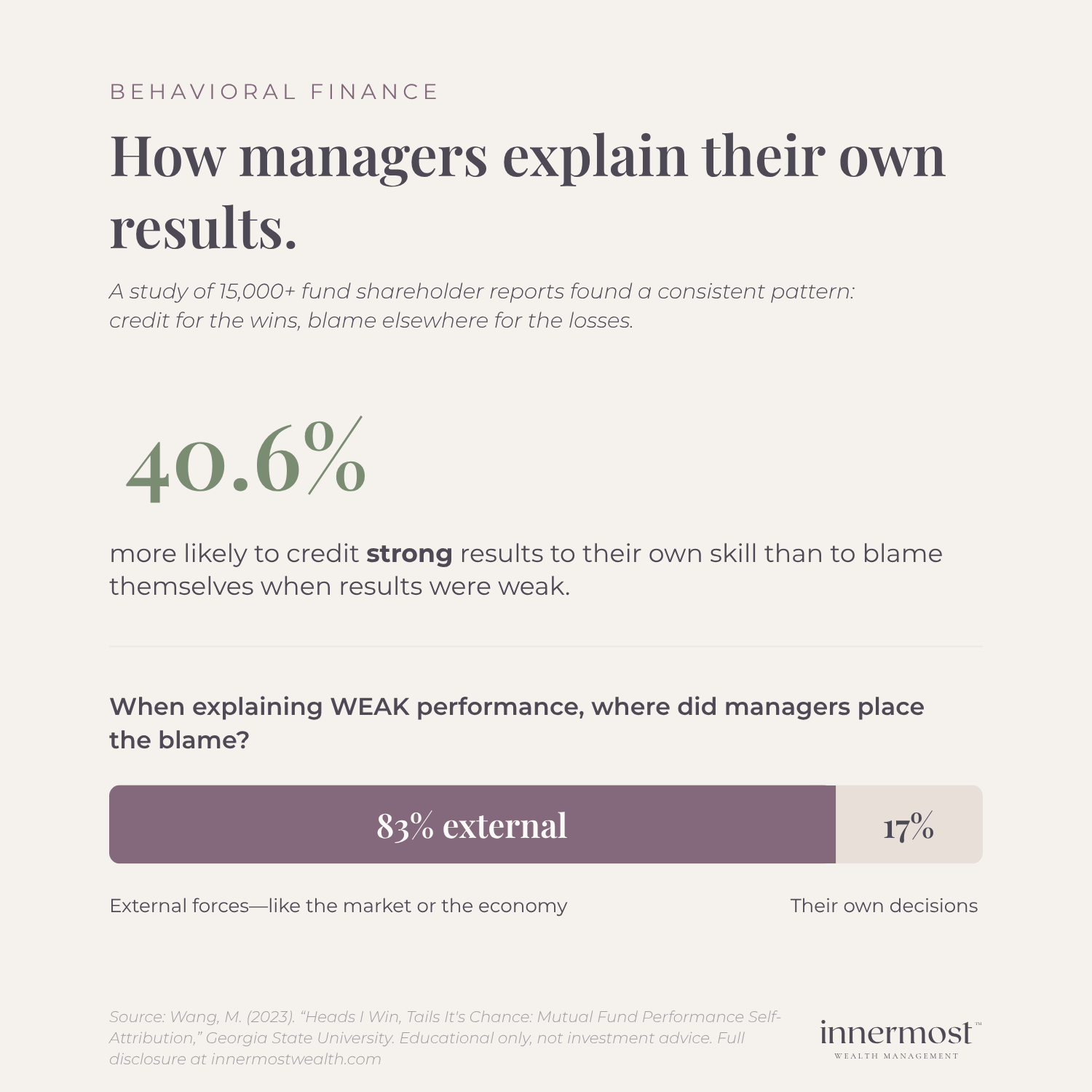

A recent academic study by Meng Wang at Georgia State University provides a revealing example of how psychological dynamics appear in the investment industry.

The research examined how mutual fund managers explain their funds' performance in official shareholder reports. Using machine learning techniques to analyze more than 15,000 regulatory filings across nearly 2,000 mutual funds, the study evaluated the language managers used when describing investment results.

The pattern was striking. Managers consistently took credit for what went right and pointed elsewhere for what went wrong:

On average, managers were 40.6% more likely to credit strong results to their own skill than they were to blame themselves when results were weak.

When explaining weak performance, 83% of the factors they pointed to were external, such as the economy or the market, versus only 17% they attributed to their own decisions.

When returns were strong, explanations frequently emphasized investment strategy, portfolio positioning, or security selection.

When results were disappointing, the discussion often shifted toward external forces such as macroeconomic conditions or unexpected market events.

Psychologists refer to this tendency as self-attribution bias.

It reflects a common human instinct to interpret success as evidence of personal ability while viewing negative outcomes as the result of external circumstances.

This bias appears across many professions. But in investing, the consequences can be particularly significant because it influences how decision-makers interpret past performance and adjust their future behavior.

The study found that fund managers exhibiting stronger self-attribution bias were more likely to:

Trade more frequently

Take greater idiosyncratic investment risk

Experience weaker future investment performance

In practical terms, that second point means managers increasingly concentrated their portfolios. Instead of maintaining diversified exposure, they placed larger bets on individual stocks or sectors they believed they understood better than the market.

It is the financial version of doubling down because you are convinced you have a unique insight others are missing.

And the results were measurable.

A one-standard-deviation increase in self-attribution bias corresponded with a decline in future investment performance relative to benchmarks. In plain language, the more a fund manager interpreted past success as personal skill rather than a mix of skill and market conditions, the more performance tended to deteriorate over time.

The mechanism is intuitive.

When past success is interpreted primarily as evidence of ability, decision-makers may become increasingly confident in their forecasts. That confidence can encourage larger or more concentrated bets.

Sometimes that conviction is justified.

But when confidence drifts into overconfidence, judgment can become distorted.

Overconfidence in Financial Decision-Making

Self-attribution bias often operates alongside another well-documented behavioral pattern: overconfidence bias.

Overconfidence occurs when individuals systematically overestimate their ability to interpret information or predict outcomes.

In financial markets, this phenomenon has been studied extensively.

One of the most influential papers in the field comes from economists Brad Barber and Terrance Odean, who analyzed the trading behavior of thousands of brokerage accounts.

Their research revealed a striking pattern. It found that investors who traded most frequently tended to earn lower net returns than those who traded less often.

The difference was meaningful.

Frequent trading introduces transaction costs, increases timing risk, and exposes portfolios to greater short-term volatility.

The findings suggested that many investors believed they could consistently identify profitable opportunities even when the evidence showed those additional trades were reducing overall performance.

Overconfidence did not simply affect how investors felt about their abilities.

It changed how they behaved.

More trading.

More attempts to time markets.

More concentrated bets.

And in many cases, lower long-term returns.

The Confidence Paradox

Confidence itself is not inherently problematic.

Financial professionals must maintain a certain degree of conviction to make decisions under uncertainty. Markets rarely provide perfect information, and investment decisions often require acting before every variable is known.

Researchers sometimes describe this relationship as an inverted-U curve between confidence and performance.

At very low levels of confidence, decision-makers may hesitate, delay action, or avoid necessary risk.

At moderate levels, confidence can support clearer thinking and decisive execution.

But beyond a certain point, additional confidence tends to reduce decision accuracy rather than improve it.

Excessive confidence can make individuals less receptive to new information, less willing to revise assumptions, and more likely to dismiss evidence that contradicts their beliefs.

In investing, that dynamic can create significant blind spots.

Some of the most costly mistakes in financial history have emerged when strong conviction prevented decision-makers from reconsidering their assumptions.

Personality and Leadership in Finance

These psychological dynamics do not only affect individual investors.

They also appear in leadership roles across the financial and corporate landscape.

Economists Ulrike Malmendier and Geoffrey Tate have studied the effects of overconfidence among corporate executives responsible for major strategic decisions.

Their research found that highly overconfident executives were more likely to:

Pursue aggressive acquisitions

Overinvest during periods of strong performance

Rely heavily on internal forecasts rather than external information

These leaders often appeared decisive and capable.

But their confidence sometimes led them to underestimate risk or overlook warning signals.

In many cases, the consequences became visible only after substantial capital had already been committed.

Although this research focuses on corporate leadership, similar psychological forces can influence investment management.

The financial industry often rewards individuals who project confidence and decisiveness. Media coverage, conference panels, and industry rankings frequently highlight bold predictions and strong personalities.

Those traits can be valuable.

But they can also amplify behavioral biases if they are not balanced by disciplined decision frameworks.

Why Finance Often Rewards Certainty

Part of the challenge lies in how financial expertise is communicated.

Clients naturally want reassurance. Markets can be volatile and emotionally taxing, and people often seek professionals who appear confident in their guidance.

Public commentary reinforces this dynamic.

Investment professionals are frequently asked to provide definitive views about where markets are heading next. Forecasts and predictions tend to attract more attention than discussions about uncertainty or probability.

Certainty can be persuasive.

But markets are inherently uncertain systems influenced by countless variables.

The professionals who sound the most confident are not always the ones making the most thoughtful decisions.

In some cases, the opposite may be true.

Some advisors focus less on predicting markets and more on designing decision frameworks that help clients navigate uncertainty.

What to Look for in a Financial Advisor

For individuals evaluating a financial advisor or investment manager, understanding these psychological dynamics can offer useful perspective.

Technical knowledge and credentials matter.

But the way financial decisions are approached may matter just as much.

Several behavioral patterns may provide insight into how a professional approaches uncertainty.

Willingness to acknowledge mistakes

Markets involve probabilities, not guarantees. Advisors who openly discuss past mistakes may demonstrate a thoughtful approach to uncertainty.

Transparency about decision frameworks

Clear processes allow clients to understand how investment decisions are formed.

Consistency of philosophy

Frequent strategy shifts can signal reactive decision-making rather than a stable long-term framework.

Intellectual humility

Professionals who acknowledge complexity tend to approach markets with greater discipline. Humility in this context reflects an understanding of how uncertain markets actually are.

The Role of Behavioral Awareness

One of the most important developments in modern finance has been the growing recognition that psychology plays a central role in financial outcomes.

Traditional economic models once assumed investors behaved as purely rational actors.

Behavioral economists such as Daniel Kahneman and Amos Tversky demonstrated that human decision-making is systematically influenced by cognitive biases, framing effects, and emotional responses.

Investors interpret information through mental shortcuts and past experiences.

Financial professionals are no different.

The goal is not to eliminate these biases entirely. That would be unrealistic.

But awareness of them can improve decision processes.

Many thoughtful investment organizations incorporate behavioral safeguards such as structured investment committees, systematic portfolio rules, and deliberate review processes designed to challenge assumptions.

In many ways, humility becomes a form of risk management.

A Different Model of Financial Leadership

The longer I work in financial planning, the more convinced I become that thoughtful financial leadership often looks different from the stereotype associated with the industry.

Markets are complex systems. Even highly skilled professionals cannot consistently predict short-term outcomes with certainty.

Some advisors who serve clients over long periods of time often share a different set of traits.

They emphasize process over prediction.

They prioritize risk management over bold narratives.

They remain open to revising assumptions when new information emerges.

And perhaps most importantly, they recognize that financial planning is not solely about investments.

It is about people.

Clients bring their family histories, life transitions, and personal values into financial decisions. These realities shape how risk is perceived and how financial choices are made.

Addressing those factors requires more than technical expertise.

It requires attention, patience, and emotional awareness.

Why This Topic Matters to Me

Part of what deepened my interest in behavioral finance and psychology early in my career was my own experience working inside the financial industry.

I studied both finance and psychology in school and had always been fascinated by how people think, make decisions, and respond to uncertainty. But as I began working in financial environments, that interest quickly became more than academic.

I found myself increasingly drawn to the research behind behavioral finance, decision-making, and personality dynamics. The more I observed how financial decisions were actually made in practice, the more I wanted to understand the psychological forces shaping those choices.

At the same time, I sometimes felt slightly out of place in traditional industry environments. The dominant model of success in finance tends to reward a particular type of personality: highly extroverted, assertive, comfortable projecting certainty, and aligned with the traditional image of authority that has long shaped the industry.

Those traits can certainly be valuable.

But over time I noticed something interesting.

Many of the qualities that make someone a thoughtful financial advisor do not always look like traditional “industry confidence.”

They often look quieter.

Listening carefully before offering advice.

Paying attention to subtle emotional cues in conversations about money.

Recognizing when fear, family history, or past experiences are shaping financial decisions.

Asking thoughtful questions before presenting answers.

In other words, the skills that build trust with clients are often the ones that receive the least attention inside the industry.

Empathy.

Curiosity.

Patience.

Emotional awareness.

For a time, I wondered whether those traits meant I simply did not fit the profession.

Eventually I realized something different.

Those qualities are not weaknesses in financial planning.

They are strengths.

Clients rarely seek financial advice because life feels predictable. They come during moments of transition: career changes, divorce, family decisions, inheritance, or uncertainty about the future.

In those moments, what people often need is not someone performing certainty.

They need someone who can listen carefully, think clearly, and guide decisions with both technical knowledge and emotional intelligence.

Final Thoughts

Finance will always involve uncertainty.

Markets rise and fall. Strategies evolve. Economic conditions shift.

But one constant remains.

The psychology of decision-makers matters.

Behavioral finance research continues to show that biases such as self-attribution and overconfidence influence how investment professionals interpret success, manage risk, and make future decisions.

For investors, understanding those dynamics provides another lens for evaluating financial leadership.

Credentials and experience matter.

But so do judgment, transparency, and intellectual humility.

In an industry built on forecasts and confident predictions, the most valuable skill may simply be the ability to approach financial decisions with humility about what cannot be known.

For investors who want to explore how behavioral awareness can inform long-term financial decisions, you’re welcome to schedule a conversation here.

Frequently Asked Questions About Behavioral Finance

-

Behavioral finance is a field of study that examines how psychology influences financial decision-making. Traditional economic models assume investors behave rationally, but behavioral finance research shows that emotions, cognitive biases, and personal experiences often influence how people evaluate risk, interpret information, and make investment decisions.

-

Overconfidence can lead investors to overestimate their ability to predict market movements or select winning investments. Research has shown that overconfident investors tend to trade more frequently, take larger concentrated bets, and underestimate risk, behaviors that can reduce long-term investment returns.

-

Self-attribution bias occurs when investors attribute successful outcomes to their own skill while blaming negative results on external factors such as market conditions or economic events. Behavioral finance research shows that this bias can increase confidence after periods of success, sometimes leading to riskier investment decisions.

-

Financial decisions are rarely based on numbers alone. Life transitions, past experiences with money, family dynamics, and personal values all influence how people think about risk and financial goals. Financial planning that incorporates behavioral awareness can help investors make more thoughtful and sustainable long-term decisions.

-

Choosing a financial advisor is about more than credentials, though those matter too. Beyond technical qualifications, it's worth paying attention to how an advisor approaches uncertainty: whether they're transparent about their decision-making process, consistent in their philosophy, and willing to acknowledge what they don't know. Markets deal in probabilities, not guarantees, so an advisor who discusses risk honestly rather than projecting certainty is often demonstrating exactly the kind of discipline that serves clients well over time. Fee structure matters as well; a fee-only fiduciary is legally required to act in your best interest.

-

A few questions can reveal a great deal about how an advisor actually works. Ask how they make investment decisions, how they've handled past mistakes, how they're compensated, and whether they're a fiduciary. Their answers tell you whether there's a clear, repeatable process behind their advice or mostly confidence and prediction. An advisor who can walk you through their framework, and who talks candidly about uncertainty rather than promising outcomes, is showing you the thinking you'll be relying on for years.

-

Several well-documented biases affect how people invest, often without their noticing. Two of the most consequential are overconfidence, the tendency to overestimate our ability to predict outcomes, and self-attribution bias, the tendency to credit success to our own skill while blaming losses on outside forces. Others include loss aversion, where the pain of a loss outweighs the pleasure of an equivalent gain, and recency bias, where recent events feel more important than they are. The pioneering work of psychologists Daniel Kahneman and Amos Tversky showed these patterns are systematic and human, not signs of poor judgment. Awareness of them is what allows for better decision processes.

Sources

Barber, B., & Odean, T. (2000).

Trading Is Hazardous to Your Wealth: The Common Stock Investment Performance of Individual Investors. Journal of Finance.

Kahneman, D. (2011).

Thinking, Fast and Slow.

Malmendier, U., & Tate, G. (2005).

CEO Overconfidence and Corporate Investment. Journal of Finance.

Wang, M. (2023).

Heads I Win, Tails It's Chance: Mutual Fund Performance Self-Attribution. Georgia State University.