The Great Wealth Transfer: Estate Planning for Multi-Generational Families

Key Takeaways

Industry research suggests trillions of dollars may transfer from older generations to heirs over the coming decades.

Estate planning for multi-generational families requires coordinated trust structures, tax strategy, and family governance.

Women are increasingly stepping into financial leadership through inheritance and should be intentionally included in planning conversations.

Thoughtful wealth transfer planning protects assets, reduces unnecessary taxes, and preserves long-term family values.

The great wealth transfer is a leadership transition.

Over the next 20 years, an unprecedented amount of wealth is expected to move from baby boomers and older generations to their children and grandchildren.

For many families, this will be the largest financial transition they have ever experienced.

Increasingly, women will inherit and manage a significant portion of this wealth. Many will become primary financial decision-makers after years of partnership or caregiving and often without having been fully integrated into prior estate planning decisions.

That is why modern estate planning must move beyond basic estate planning documents.

Multi-generational estate planning refers to the coordinated legal, tax, and financial strategies used to transfer wealth across multiple generations while preserving family values, minimizing unnecessary taxes, and preparing future decision-makers.

It is not simply about distributing assets. It is about designing continuity.

Estate planning begins with intent, not paperwork.

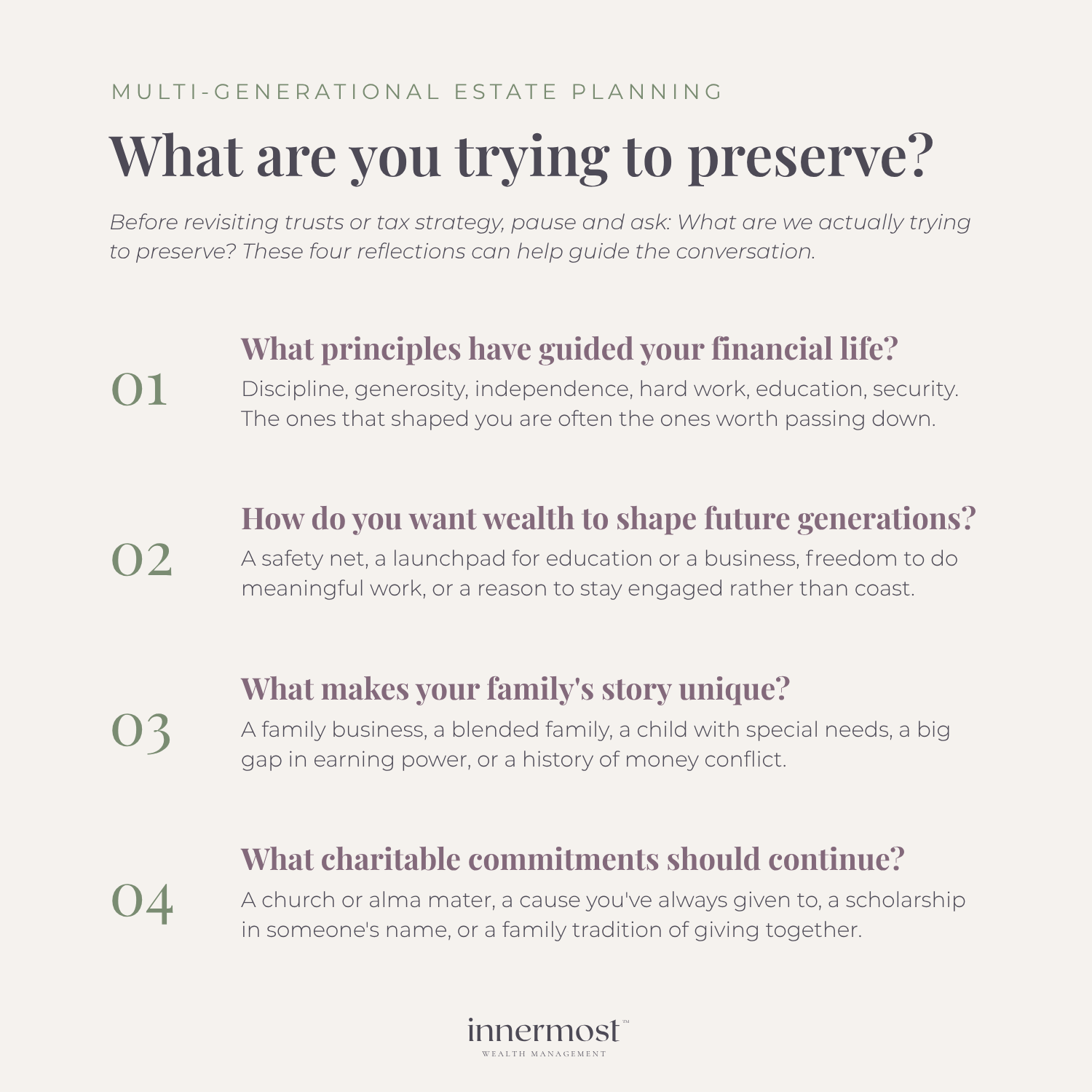

Before revisiting trust structures or tax strategies, pause and ask a deeper question:

What are we actually trying to preserve?

For some families, it is entrepreneurial drive. For others, it is education, philanthropy, independence, or resilience.

Estate planning that focuses only on tax minimization often misses this layer.

Consider reflecting on:

What principles have guided your financial life?

How do you want wealth to shape future generations?

What unique circumstances exist within your family (business ownership, divorce, special needs, unequal earning power)?

What charitable commitments should continue beyond your lifetime?

These answers become the blueprint for how legal structures are designed. Tax efficiency matters, but understanding and defining the intent is important.

Understanding the current estate tax landscape.

Federal estate tax exclusion amounts remain historically elevated; however, exemption levels are subject to legislative change. Future tax law developments are uncertain and depend on congressional action.

For families with significant assets, proactive planning may include:

Strategic lifetime gifting

Utilizing annual exclusion gifts

Funding irrevocable trusts

Leveraging generation-skipping transfer (GST) exemptions

Coordinating charitable strategies

Planning during favorable tax environments may preserve flexibility and expand available options.

Importantly, estate tax planning and probate avoidance are not the same. A plan can avoid probate yet still create unnecessary estate tax exposure if not structured properly. This distinction matters.

Estate planning strategies should be implemented in coordination with a qualified estate planning attorney and tax professional.

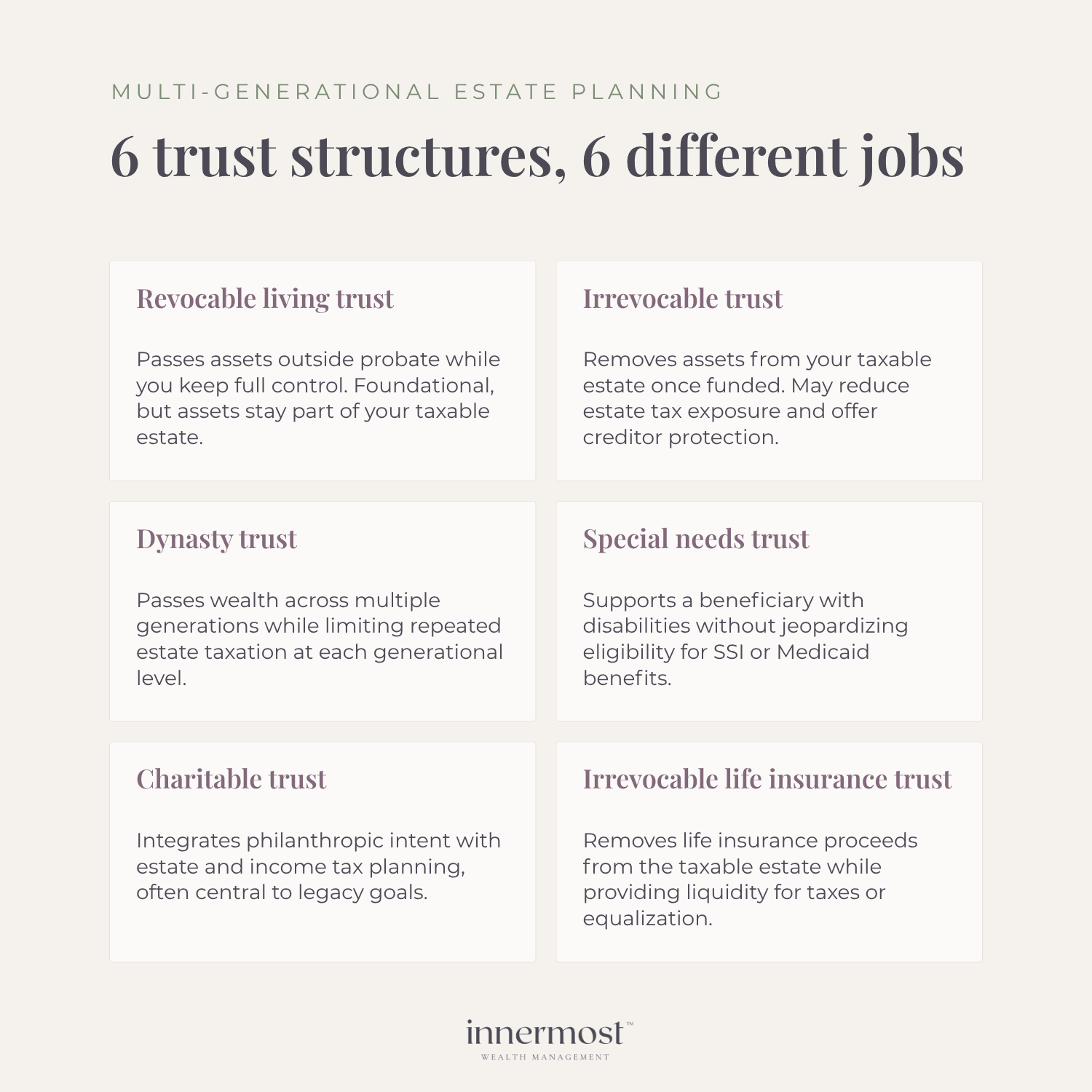

Trust structures used in multi-generational estate planning.

Trusts are often central to preserving wealth across generations. Each serves a different function.

Revocable Living Trust

A revocable living trust allows assets to pass outside of probate while you retain full control during your lifetime.

It improves administrative efficiency and privacy. However, assets in a revocable trust remain part of your taxable estate and are generally not protected from creditors.

For many families, this is foundational but not sufficient planning.

Irrevocable Trust

An irrevocable trust removes assets from your taxable estate once properly structured and funded.

These trusts may:

Reduce estate tax exposure

Protect appreciating assets from future estate taxation

Provide creditor protection depending on structure and jurisdiction

Irrevocable trusts require thoughtful drafting because they limit your ability to modify terms later.

Dynasty (Generation-Skipping) Trust

A dynasty trust allows assets to pass across multiple generations while minimizing repeated estate taxation at each generational level.

When thoughtfully structured and coordinated with GST planning, this type of trust may help preserve family capital across generations.

For families seeking long-term continuity, this structure is often a powerful tool.

Special Needs Trust (SNT)

A special needs trust allows a beneficiary with disabilities to receive support without jeopardizing eligibility for government benefits such as SSI or Medicaid.

Without proper planning, a direct inheritance could unintentionally disqualify a loved one from essential support programs.

Precision matters here.

Charitable Trusts (CRT / CLT)

Charitable remainder and charitable lead trusts integrate philanthropic intent with estate and income tax planning.

For many women in particular, philanthropy is deeply connected to identity and legacy. Structuring charitable giving intentionally can help support long-term philanthropic goals.

Irrevocable Life Insurance Trust (ILIT)

An ILIT can remove life insurance proceeds from the taxable estate while providing liquidity for estate taxes, business equalization, or asset distribution.

Liquidity planning is often overlooked. Estate tax bills are due in cash even if wealth is held in businesses or real estate.

Preparing women for financial stewardship.

A growing share of inherited wealth will move into the hands of women.

Yet many women are not included early enough in estate planning conversations.

This is where psychology and planning intersect.

Preparation changes the experience of inheritance.

When women are included as decision-makers rather than simply beneficiaries, they gain the context and confidence needed to step into financial stewardship. Estate planning becomes intentional instead of reactive.

Intentional multi-generational planning should include:

Transparent discussions about asset structure

Education around trust mechanics

Participation in philanthropic decisions

Clear explanation of tax implications

Wealth without preparation creates pressure. Wealth with preparation creates stability.

Incentives, motivation, and the psychology of inheritance.

One of the most common concerns among affluent families is whether inheritance will undermine drive.

Trust provisions can align distributions with demonstrated responsibility, such as:

Education milestones

Income-matching structures

Entrepreneurial funding

Philanthropic participation

Demonstrated financial literacy

However, guardrails must be balanced.

Too much restriction can feel controlling. Too little structure can feel destabilizing.

Money carries emotional weight in families. Estate structures should acknowledge that reality rather than ignore it.

If you’re on the receiving end of a wealth transfer, this guide on what to do with an inheritance walks through the financial and emotional decisions that come next.

Business succession planning requires coordination.

For families with closely held businesses, estate planning becomes more complex.

Questions to address include:

Will ownership and management remain aligned?

Are all heirs equally involved in the business?

Is there liquidity available to cover estate taxes?

Are buy-sell agreements properly funded?

How will governance transfer?

Business succession planning must integrate with trust structures, tax strategy, and investment planning. Without coordination, transitions can create internal conflict or forced asset sales.

With planning, they create continuity.

Family governance: the missing layer.

Legal documents alone do not teach stewardship.

Family governance often includes:

A written mission or legacy letter

Structured family meetings

Defined trustee roles

Gradual delegation of responsibility

Ongoing financial education

Many families avoid discussing wealth out of fear that transparency will create entitlement.

In practice, secrecy often creates confusion.

Age-appropriate conversations build resilience. Stewardship is learned through exposure, not silence.

Integrating multi-generational estate planning with your financial plan.

Estate planning is most effective when integrated with:

Liquidity strategy

Philanthropic goals

An estate plan should not sit in isolation from your financial life.

At Innermost Wealth Management, multi-generational estate planning is approached as part of comprehensive financial planning, aligning tax modeling, investment strategy, and family governance.

The emotional reality of wealth transfer.

Inheritance often occurs during grief.

Administrative complexity including probate filings, trust management, and tax returns can intensify emotional strain.

Thoughtful estate planning reduces that burden.

It protects surviving spouses, often women, from navigating complexity alone.

Planning ahead is an act of love.

Final thoughts.

The great wealth transfer is not simply about passing down assets.

It is about transferring leadership, responsibility, and values.

Multi-generational estate planning ensures that wealth strengthens future generations rather than destabilizing them.

When thoughtfully designed, estate strategies preserve not only financial capital, but family culture and long-term independence.

Frequently asked questions about multi-generational estate planning.

Estate planning for multi-generational families often raises questions that go beyond a basic will. Below are a few of the conversations we frequently have with families navigating long-term wealth transitions.

-

The “great wealth transfer” refers to the projected movement of trillions of dollars from older generations to their children and grandchildren over the coming decades. As life expectancies increase and asset values grow, this transfer is expected to reshape financial leadership within many families, particularly as more women step into primary wealth stewardship roles.

-

Estate tax exposure may be reduced through coordinated planning strategies such as lifetime gifting, irrevocable trusts, generation-skipping transfer (GST) planning, charitable trust structures, and liquidity planning.

However, not all families face federal estate tax liability. The appropriate strategy depends on asset size, asset type, state-level tax considerations, and long-term goals.

-

Estate plans should be reviewed after major life events (marriage, divorce, birth of a child, business sale, inheritance) and periodically as tax laws evolve.

Even when no major event occurs, reviewing estate documents every few years ensures that trust structures, beneficiaries, and tax assumptions still align with your financial plan and family dynamics.

-

A will directs how assets are distributed but generally requires probate. A trust can provide additional benefits such as probate avoidance, privacy, structured distributions, and in certain cases estate tax efficiency or creditor protection.

Whether a trust is appropriate depends on the complexity of your assets, tax exposure, and long-term planning objectives.

-

Women are increasingly stepping into control of significant assets, often after the loss of a spouse. Intentional estate planning can ease administrative strain during emotionally heavy seasons and support confident, informed financial leadership.