What to Do With an Inheritance: A Guide to Honoring the Past and Planning Your Future

Key Takeaways

An inheritance should be integrated into your overall financial plan, not treated as separate or “extra” money

Taking time before making decisions can help avoid costly mistakes and improve long-term outcomes

Tax considerations, including inherited retirement accounts and capital gains, can significantly impact your strategy

Consolidating accounts and organizing assets can make decision-making clearer and more effective

Working with the right professional can help reduce complexity and create a structured, thoughtful plan

Nobody tells you this about inheriting money.

The hard part isn't the investing.

It's the Tuesday afternoon when you're staring at a statement from an institution you've never heard of, trying to figure out if you're supposed to do something with it, while also just missing the person who left it to you.

That's where most people actually are when they first sit down with us. Not confused about asset allocation. Confused about how to even begin.

And if that's where you are right now, this is for you.

First: What to Do When You Receive an Inheritance

When someone inherits money, one of two things tends to happen almost immediately.

They rush. They feel the pressure to be responsible, to honor the person, to not mess this up. And so they make decisions before they've had a chance to breathe, let alone think. Or they freeze. The paperwork sits on the counter. The voicemails from the financial institution go unreturned. Weeks become months.

Both responses make complete sense. Grief does that. Big decisions do that. Grief and big decisions at the same time? Your nervous system was not designed for that.

There's a concept in behavioral finance called decision fatigue under emotional load. Basically, when we're grieving or stressed, the part of our brain responsible for long-term planning goes offline. We're wired to either act impulsively or shut down entirely. Neither is a character flaw. Both are just beautifully, painfully human.

“The first thing I tell people when they are trying to figure out how to handle an inheritance is this: park the money somewhere safe. Breathe. The markets will still be there in 30 days.”

Placing the funds in a stable, liquid account while you find your footing is not procrastination. It is the most strategic thing you can do. Because the quality of every financial decision you make from here will be better if you make it from a place of stability and peace rather than pressure.

Navigating the Rules and Tax Treatment of Inherited Assets

An inheritance is rarely just a check. It can include:

Brokerage or investment accounts

Retirement accounts like IRAs or 401(k)s

Real estate

Life insurance proceeds

Personal assets that carry both financial and emotional value

Each of these comes with its own rules, timelines, and tax treatment. And the rules are not always obvious. Many of these complexities are shaped by how the estate was originally structured. If you're curious how these decisions are made ahead of time, this overview of multi-generational estate planning explains how wealth is intentionally transferred across generations.

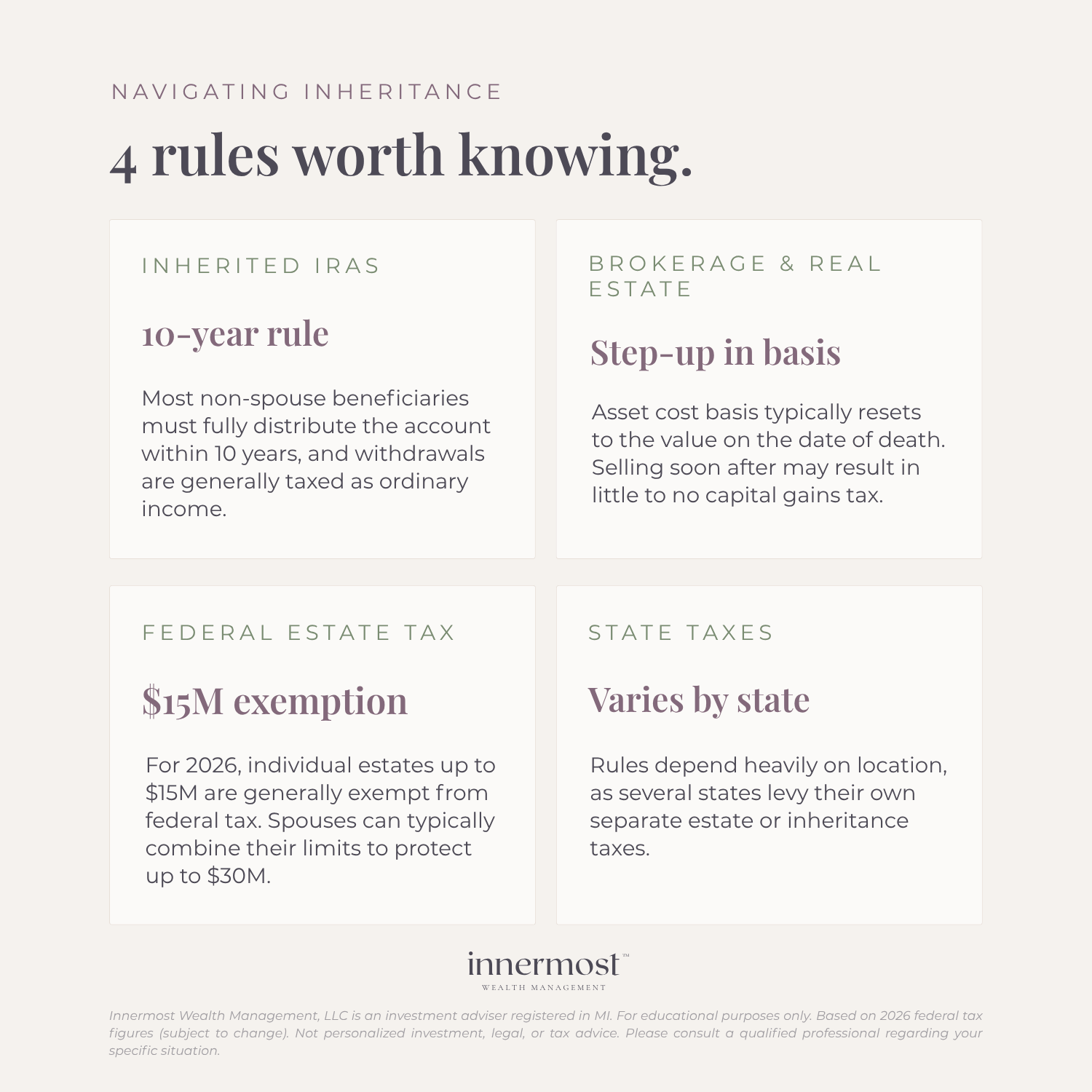

Inherited IRAs, for example, have distribution requirements that most people don't know about until they're already behind on them. Under current IRS rules, most non-spouse beneficiaries are required to fully distribute an inherited retirement account within 10 years. Miss that window and there are penalties.

Taxable brokerage accounts work differently. They may receive what's called a step-up in cost basis, which resets the taxable gain to zero as of the date of death. That can change everything about whether it makes sense to sell immediately or hold.

Real estate has its own situation entirely. Ongoing costs, potential rental income, shared ownership with other beneficiaries, and capital gains implications all come into play.

None of this is insurmountable. It just needs to be understood before it's acted on. And it's a lot to untangle when you're also grieving.

If you’re navigating multiple accounts, tax considerations, or family decisions, this is often where having a structured plan can make a meaningful difference. Reach out to us today to schedule a free consultation.

The Money Psychology and Emotional Side of Inherited Wealth

Let's stay here for a minute, because I think it matters.

There is a hidden layer to inheriting wealth that traditional financial guides almost never address, yet it is the exact layer that quietly drives most major financial decisions, for better or worse. When an account changes hands, we don't just inherit capital; we inherit a complex web of emotions, expectations, and historical family dynamics.

First, there is the silent weight of guilt. It is incredibly common to feel like the money isn't truly yours, or to experience a paralyzing sense of pressure because those dollars represent someone else's entire lifetime of sacrifice, sweat, and work. Suddenly, a simple investment choice feels like a high-stakes test of how well you are honoring their memory.

This frequently triggers a unique form of financial imposter syndrome. It can surface even in individuals who are wildly successful and capable in every other area of their lives. Facing a sudden influx of wealth can make you feel ill-equipped, as if you are merely a temporary custodian waiting to make a wrong move.

We must also recognize that money stories get inherited right alongside the actual assets. If the person who left you this money was deeply secretive about finances, or if you were historically kept out of financial decisions in your family or a past partnership, those ingrained psychological scripts do not vanish when the assets hit your account. Those old patterns reappear, dictating how you save, spend, or avoid the money entirely.

Furthermore, for couples navigating an inheritance together, the transition acts as a stress test for the relationship. It abruptly forces to the surface differing money values, unspoken risk tolerances, and competing priorities that may have never been fully examined before.

“Managing an inheritance touches something infinitely deeper than mechanical financial literacy. It touches your entire relationship with money, and ultimately, your relationship with the person who left it behind.”

This isn't a therapy problem, but it is also not a riddle that a spreadsheet can solve on its own.

It is why the financial planning frameworks I build are deliberately designed to hold both pieces at once: the cold, technical complexities of tax and portfolio architecture, and the deeply human experience unfolding underneath them. Because when those two realities are addressed together, the financial decisions you make don’t just look good on paper, they actually stick.

Defining Your Goals Before Allocating an Inheritance

What do I actually want this money to do?

Not what should I do with it. Not what would the person who left it want. Not what sounds most responsible.

What do you want?

For some people, the answer is security. The inheritance represents a chance to finally feel financially stable, to pay off debt, to build a cushion that has never existed before.

For others, it's flexibility. The ability to make a career change, support a child's education, or stop deferring a decision that has been on hold for years.

For some, there's a relational dimension. The money carries meaning tied to the person who left it, and deciding how to honor that without being paralyzed by it is part of the work.

There is no universal right answer. But decisions that are connected to a clear sense of purpose tend to hold up better over time than decisions made out of pressure or obligation.

This is usually where the most important conversation starts.

How to Manage an Inheritance: A Step-by-Step Approach

Before deciding what to do next, it can be helpful to understand how this wealth was structured to be passed down in the first place.

Once you have some clarity on the why, the what gets a lot easier to navigate. Here are the directions most people explore:

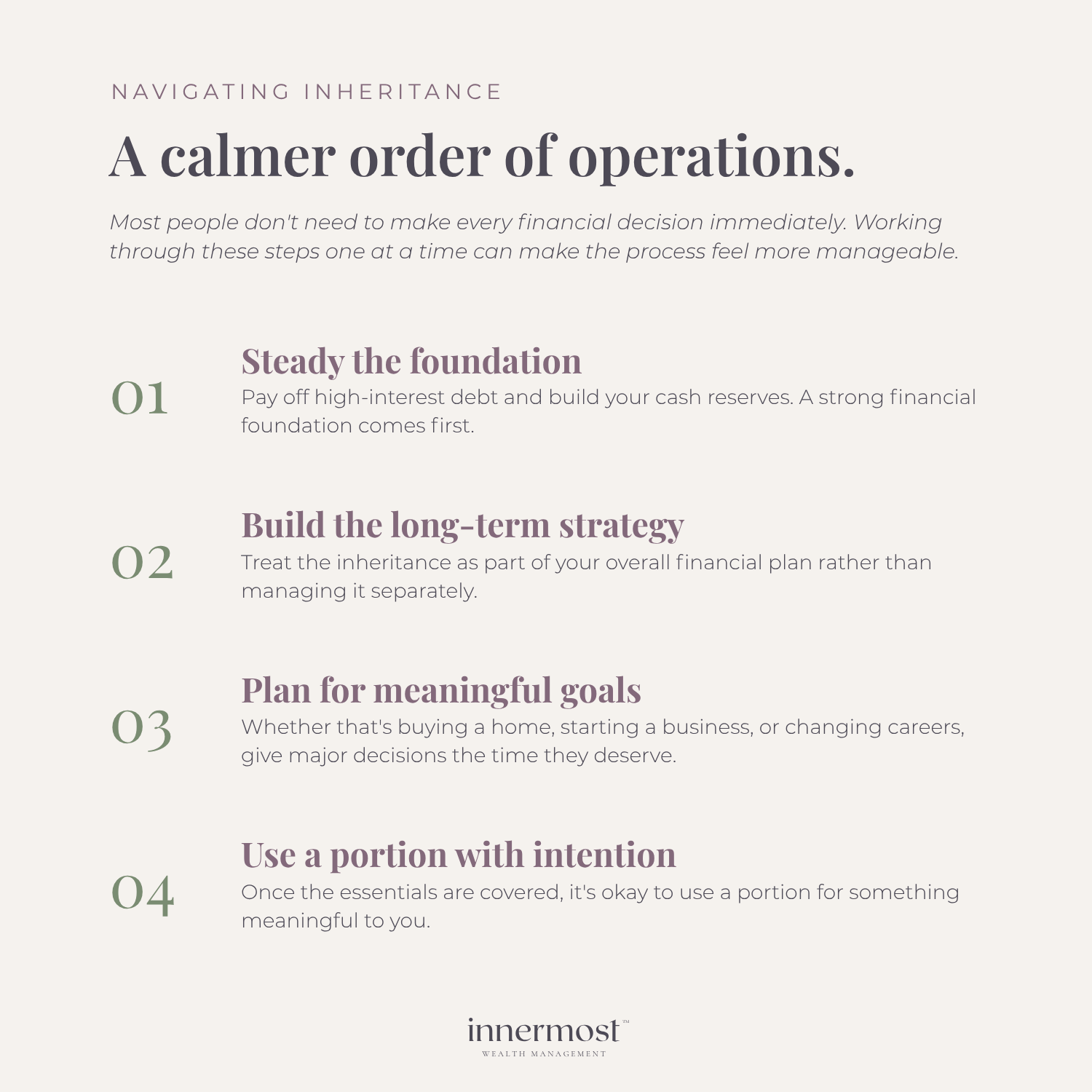

Step 01

Manage the immediate foundation (debt & cash reserves).

Paying off high-interest debt or filling gaps in your emergency fund creates stability that ripples through every other financial decision. It also reduces the psychological weight of financial fragility, which is its own kind of freedom.

Step 02

Build a long-term inheritance investment strategy.

An inheritance can become a meaningful part of a long-term portfolio, particularly when it's evaluated within the context of everything else you have going on rather than managed as a separate pot of money. The sequencing of when you invest, how you invest, and how it's structured for taxes matters more than most people realize.

Step 03

Plan for meaningful goals.

Sometimes an inheritance makes it possible to move forward with something that would otherwise have taken years: buying a home, funding a business, creating flexibility around work. These decisions carry both financial and personal weight, and they benefit from being evaluated carefully rather than rushed.

Step 04

Use a portion with intention.

Once the foundation is secure, the long-term strategy is set, and major life goals are accounted for, the final step is giving yourself permission to use a specific portion of the wealth right now. Many people want to set something aside in a way that reflects the person who left it. For example, a shared family experience, a charitable contribution, or a meaningful purchase. Approaching this as a deliberate, bounded choice helps you honor that impulse without letting emotion override the entire financial plan.

The Tax Implications (Understanding the Nuances)

Taxes can significantly affect what you ultimately retain, and the decisions made during the first year or two can have long-term structural implications.

Here are several key considerations to keep in mind:

Under current law and the time of this writing, for most people there may not be federal inheritance tax. Federal estate taxes kick in above $15 million per individual, so unless the estate was very large, this likely isn't a factor.

State taxes are a different story. Many states have their own estate or inheritance taxes at much lower thresholds. Whether you owe depends on where the deceased lived, not necessarily where you live.

Inherited IRAs create taxable income. Distributions are taxed as ordinary income, and under the 10-year rule, how you time those withdrawals can meaningfully affect your tax bill each year.

The step-up in basis is one of the most valuable and least understood tax provisions in inheritance law. If you inherit a brokerage account, the cost basis resets to the value on the date of death. Selling immediately might trigger almost no capital gains tax, even on an account that grew significantly over decades.

Real estate also gets the step-up, but ongoing ownership adds complexity. Depreciation recapture, rental income, and future appreciation all factor in.

The timing of when you liquidate, distribute, or reinvest inherited wealth can have substantial financial impacts. Because tax laws are complex and subject to change, it is critical to coordinate these decisions with both a qualified financial planner and a certified tax professional.

Managing an Inheritance with Siblings: Handling Shared Property

If you’re sharing this inheritance with siblings, a co-parent, or other family members, I want to be honest with you: this is where things can get complicated fast. Wealth transition has a unique way of acting like a magnifying glass—whatever underlying friction, unspoken communication patterns, or unresolved dynamics existed in the family before will suddenly be brought into sharp, high-stakes focus.

Everyone comes to the table with entirely different financial realities, different personal timelines, and distinct emotional relationships to both the money and the person who left it. A shared piece of real estate, in particular, can surface profound disagreements that were never there before.

One person wants to sell and diversify. Another wants to keep the property as an emotional anchor to the past. A third might be facing an immediate liquidity need that the others don't fully understand.

None of these positions are wrong; they are simply different. But while separating objective financial analysis from deep-seated emotional dynamics is a heavy lift for any family under the best of circumstances, it can feel nearly impossible when grief is sitting at the table. Grief changes the gravity of every conversation. It amplifies old childhood roles, shortens tempers, and quietly transforms a standard logistical puzzle into an emotional minefield.

When navigating shared assets, the paths forward usually fall into a few categories: a total sale and clean distribution of cash, a structured buyout where one party acquires the others' shares, or a formalized shared ownership framework governed by a strict legal agreement.

Understanding what each person actually needs—whether that is financial security, validation, or simply time to process—is what ultimately points toward a resolution that protects both the wealth and the family relationships. Because these decisions are so highly individualized, it is often best for each family member to work with their own financial advisor or professional team. This ensures everyone is fully informed, respects personal boundaries, and allows the family to collaborate objectively to find the best possible path forward.

Professional Inheritance Management: What Good Planning Looks Like

I want to be direct about this, because I think it's often misunderstood.

The value of working with an advisor on an inheritance isn't primarily about investment selection. It's about having someone who can hold the whole picture at once.

That means:

Organizing accounts that are spread across multiple custodians and platforms

Understanding the rules and timelines for each type of asset

Sequencing decisions so that earlier choices don't create problems later

Coordinating the tax strategy across the full picture

Holding space for the emotional weight of the process, not just the technical complexity

For most people, this isn't just about getting the numbers right. It's about being able to move through this process without feeling like you're carrying it alone.

And that, honestly, is what changes the experience.

A Few Patterns Worth Knowing About

After working with a lot of people through this, a few things come up consistently. Not as mistakes, just as very understandable human responses to a hard situation:

Acting before fully understanding what you have. Especially with inherited retirement accounts, where the distribution rules carry real consequences.

Managing the inheritance separately from the rest of your financial life. It's its own account, so it feels like its own thing. But decisions made in isolation often create problems elsewhere.

Indefinite delay. Not because you don't care, but because engaging with the paperwork means engaging with the loss. This is one of the most common patterns, and one of the most costly.

Letting obligation drive the plan. Feeling like you have to preserve everything, or invest it exactly how the person would have wanted, to the point where the money never actually serves your own life.

Recognizing these patterns in yourself is not a reason for self-criticism. It's just useful information. And most of them resolve quickly with the right structure and someone in your corner.

You Don't Have to Figure This Out All at Once

That's really what I want you to take from this.

An inheritance is not a test you pass or fail. It's a process. And it tends to go better when it's treated like one.

The people who navigate this well aren't the ones who acted fastest or knew the most going in. They're the ones who gave themselves permission to slow down, get organized, and make decisions from a place of clarity rather than pressure.

That's available to you too.

If you're in the middle of this and want help thinking it through, we’d love to talk.

We can start wherever you are. No pressure to have it figured out before we speak.

Frequently Asked Questions About Inheritance & Multi-Generational Wealth

-

When you receive an inheritance, the first step is usually to pause before making major financial decisions.

Many people feel pressure to act quickly or avoid dealing with it altogether. Both are normal, especially when the inheritance is tied to loss.

Taking time to understand the inherited assets, tax implications, and how everything fits into your broader financial life tends to lead to better long-term decisions.

-

Whether you should invest an inheritance or pay off debt depends on your overall financial situation.

High-interest debt is often a priority, but inherited money works best when it’s evaluated as part of your full financial picture rather than treated as separate or “extra.”

The right decision usually comes from understanding how that money supports your long-term goals, not just solving one piece in isolation.

-

Yes, inherited accounts can often be consolidated, but it depends on the type of asset and custodian rules.

Many people end up with accounts spread across multiple institutions, which can make decision-making harder than it needs to be.

Bringing everything into one place can improve visibility and make it easier to evaluate your options with more clarity.

-

When multiple people inherit the same asset, decisions usually need to be coordinated.

For example, inheriting a home with siblings or other beneficiaries often requires agreement around whether to sell, buy each other out, or maintain shared ownership.

These situations are often less about the math and more about aligning different needs, timelines, and perspectives.

-

Estate planning is how wealth is structured to be passed down, including decisions around trusts, taxes, and distribution.

An inheritance is what you receive and how you manage those assets afterward.

Many of the decisions you’re navigating as a beneficiary are shaped by how the estate was originally designed. If you want to better understand how these strategies are put in place ahead of time, this guide to multi-generational estate planning walks through how wealth is intentionally transferred and structured across generations.