How to Talk About a Prenup With Your Partner

Key Takeaways

A prenuptial agreement conversation should build on existing financial transparency, not introduce it for the first time

How each partner engages in the conversation often matters more than the outcome

Differences in perspective are normal. What matters is willingness to stay in it

Financial planning can ground the conversation in real numbers, not just abstract fears

Having this conversation early reduces complexity, tension, and ambiguity later

There are a few conversations in a relationship that feel heavier than they should.

Talking about a prenuptial agreement is one of them.

Not because the conversation is inherently difficult. But because of what it seems to imply.

Trust. Fairness. What happens if this doesn't go the way you're planning.

If you've built something (a career, a business, a portfolio) and you're now thinking about marriage, you're probably carrying two things at once: genuine excitement about what you're building together, and a quiet awareness that you have real assets to protect.

That tension is completely normal. And it doesn't mean you're not committed.

It means you're paying attention.

Why Prenuptial Agreement Conversations Feel So Charged

Money carries meaning that goes far beyond numbers.

It reflects how you were raised, what security looks like to you, how you make decisions, and what you believe you deserve. When you bring up a prenuptial agreement, you're not just introducing a legal document. You're bringing those underlying beliefs into the open, sometimes for the first time.

That's why the reaction isn't always about the prenup itself.

It can show up as hesitation. Defensiveness. A sense that something deeper is being questioned like the relationship, or your intentions, or how much you actually trust each other.

For many couples, this is the first time those topics surface directly.

In practice, the couples who move through this most effectively aren't the ones who avoid those reactions. They're the ones who can acknowledge them and stay in the conversation anyway.

What Is a Prenuptial Agreement?

A prenuptial agreement is a legal contract that outlines how financial matters would be handled if the marriage were to end.

At its most basic, a prenup can address:

Assets brought into the marriage

Debt

Business ownership or equity

Future income or distributions

But in practice, prenuptial agreements often go much further. This is where they become genuinely useful for women with established careers, assets, or equity compensation.

Depending on the couple and the state, a prenup can address:

How future earnings are treated during the marriage

How investment accounts or real estate are titled and divided

How equity compensation, RSUs, or business growth is handled over time

Whether and how spousal support would be structured

How certain assets are defined as separate versus marital property

How inheritances or family wealth are treated if kept separate or intentionally combined

What happens when separate and joint finances begin to overlap over time

Some prenuptial agreements are relatively straightforward. They focus primarily on protecting premarital assets. Others are more nuanced, reflecting how a couple wants to approach fairness, contribution, and decision-making across the full arc of a marriage.

There are limits to what a prenup can control. Certain provisions, particularly around child custody and support, are generally not enforceable. But the process of working through the agreement often surfaces broader questions about expectations, roles, and how financial decisions will be made together.

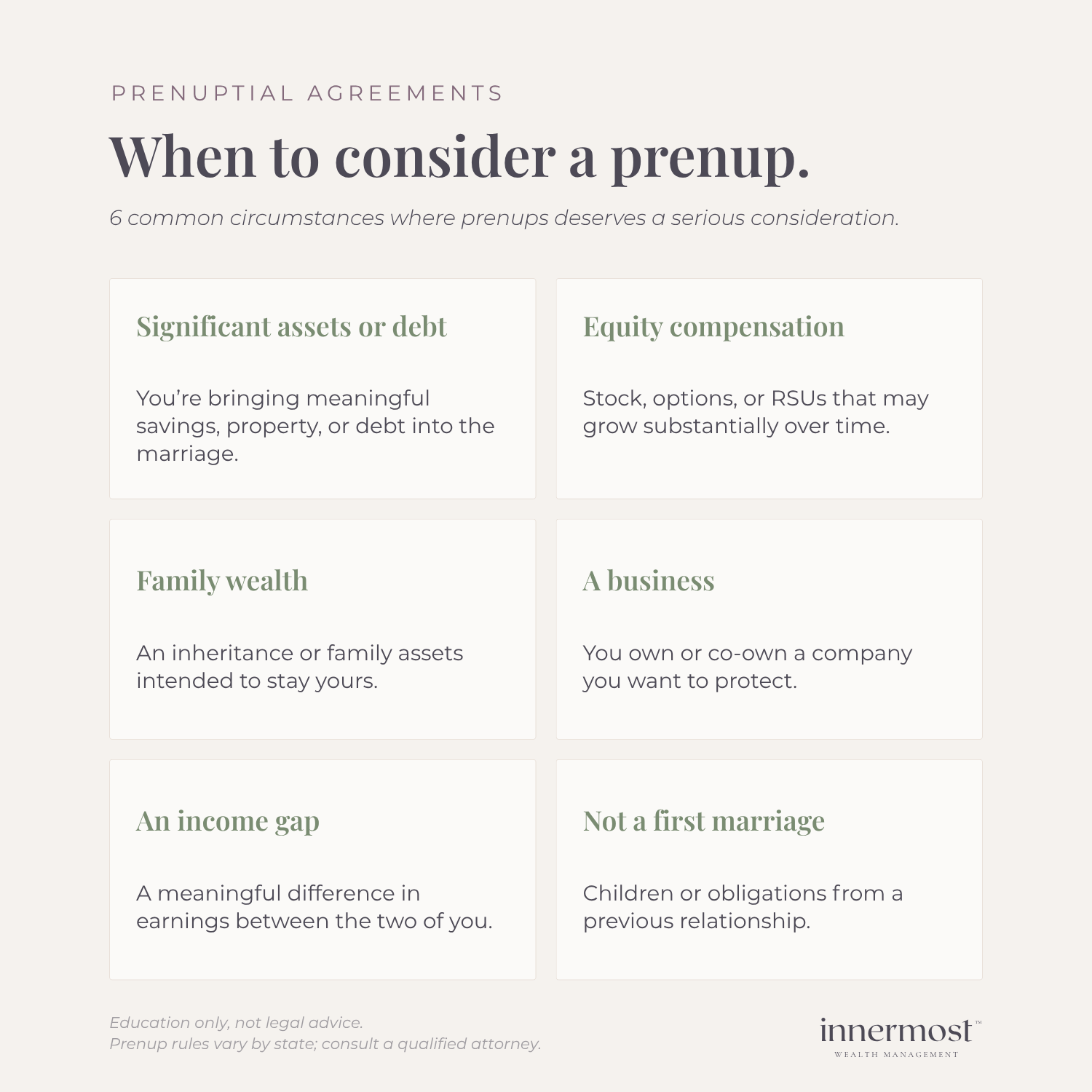

When to Consider a Prenup

My honest view: most couples benefit from having this conversation, regardless of their starting point. Not because every relationship is at risk, but because clarity tends to create stronger, more intentional foundations.

That said, there are specific situations where a prenuptial agreement becomes especially important to think through carefully.

This conversation is particularly worth having if:

You have significant assets, investments, savings, or debt going into the marriage

You have equity compensation — RSUs, stock options, or a carried interest

You own a business, or your compensation is tied to future business growth

There is family wealth or an expected inheritance you want to keep separate

There is a meaningful difference in income or net worth between you and your partner

This is not a first marriage

These situations carry more financial and structural complexity. Without clear expectations in place, it can be genuinely difficult to navigate decisions later in a way that feels fair to both people.

From a planning perspective, I tend to be more protective here, particularly for women. And given my education and experiences in divorce financial planning.

It's not uncommon for one partner to step back from their career at some point, take on more household or caregiving responsibilities, or simply have a different financial trajectory going into the relationship. Those dynamics have real long-term financial consequences, even if they feel theoretical early on.

A prenuptial agreement that's thoughtfully constructed can reflect both partners' contributions. Not just at the beginning, but throughout the marriage.

Before the Prenup Conversation, There Should Already Be Financial Transparency

In my view, a prenuptial agreement conversation should never be the first time you're learning the basics of your partner's finances.

By the time you're engaged or seriously considering a long-term commitment, there should already be a general working understanding of:

Income

Assets and debt

Spending habits

How each of you thinks about money

That doesn't mean everything needs to be organized or finalized. It does mean you're not walking into a major financial and legal conversation without context.

If a prenup introduces information that feels new or surprising, that's usually a signal the conversation is happening later than it needed to.

I'll admit, I'm biased here. I'm a financial planner, so money tends to come up early and often in my world. I know that's not most people's experience. There's still a strong social norm around keeping finances private, especially in the early stages of a relationship.

I just don't think that norm serves people well.

Money touches nearly every major decision in a shared life. When it isn't discussed early, it tends to show up later in more complicated moments such as an engagement, a large purchase, or a conversation that already has enough emotional weight on its own.

Why Power Dynamics Show Up in This Conversation

The prenuptial agreement conversation often surfaces dynamics that have been present in the relationship, but not explicitly named.

If you're entering the marriage with more assets, a higher income, or family wealth, that difference doesn't just sit on a balance sheet. It tends to influence how decisions get made. Sometimes subtly, sometimes not.

Some couples are already navigating this openly. Others are still figuring out whose voice carries more weight in financial decisions, even if that was never the intention.

A prenup conversation brings those patterns into focus.

That can feel uncomfortable. It can also be clarifying by creating an opportunity to define how decisions will actually be made going forward, rather than relying on assumptions that haven't been tested yet.

Couples who can recognize and name these dynamics tend to move through the conversation with more clarity, and less friction.

How to Discuss a Prenup

How you introduce this conversation often matters as much as what you say.

If it feels like something you've already decided and are now presenting to your partner, it can create tension almost immediately. If it's avoided entirely, it tends to build pressure and surface in a more stressful moment later.

A more grounded approach is to be intentional about the when and the how.

Rather than raising it in passing or during an already-charged conversation, it can help to create space for it. Set aside time. Go out to dinner. Order your favorite takeout. Come to it as something you're figuring out together, not something being handed to the other person.

That shift alone can change how it's received.

The framing matters, too.

This is not one person asking for something from the other. It's two people trying to figure out how to structure their financial life together in a way that feels fair, clear, and sustainable over the long term.

When the conversation shifts from "this is what I want" to "how do we want to approach this together?" it starts to feel less like opposing sides, and more like a shared problem you're working through.

Language that can help:

“I’ve been thinking about how we approach our finances long-term, and I want to make sure we’re actually aligned before we get married.”

“I think it would be helpful to talk through expectations now, when there’s no pressure to resolve anything quickly.”

This keeps the focus on the relationship, not the document.

It also helps to be realistic about the process. This is not something that gets resolved in one conversation. It's a series of conversations that build on each other. The couples who move through this most smoothly aren't the ones who immediately agree. They're the ones who stay open, keep asking questions, and are willing to understand how the other person thinks, even when it's different.

What to Pay Attention to When You Bring It Up

The outcome of the conversation matters. But in my experience, how each person engages tends to matter more.

A few things worth noticing:

Openness to the conversation

If both people are willing to engage, ask questions, and stay present, that's a strong foundation. If the topic is consistently avoided or shut down, that's worth paying attention to. Not as a verdict, but as information.

Willingness to share financial information

A prenuptial agreement requires transparency. If one person is hesitant to share basic financial details, it introduces friction into the process and signals that more foundational groundwork may need to happen first.

How fairness gets defined

Couples don't need to define fairness identically. They do need to be able to talk about it openly. When both people feel heard in that conversation, the process tends to go better.

The tone

If the conversation becomes rigid or one-sided early, it can set a pattern that carries into broader financial decisions throughout the marriage. These early moments matter.

A big part of what makes this conversation go well is whether both people feel safe being honest. If someone feels like they'll be judged or shut down, they're more likely to disengage and the conversation stops moving forward.

That's not necessarily a reflection of the relationship as a whole. But it can signal that the environment around the conversation doesn't feel fully supportive yet.

What Happens When This Conversation Is Avoided

Some couples choose not to have it at all.

Sometimes everything feels aligned and there doesn't seem to be a need. Other times, raising it feels unnecessary or disruptive to an otherwise good thing.

In the short term, avoiding it can feel easier.

Over time, it tends to create ambiguity. And ambiguity has a way of surfacing at the worst possible moments. Without clear conversations about financial expectations, couples often fill the gap with assumptions. Those assumptions may not become visible until a real decision needs to be made.

By then, the conversation carries far more weight than it would have earlier.

This doesn't mean every couple needs a prenuptial agreement.

It does suggest that conversations about money and expectations are more productive when they happen before there's pressure to resolve anything quickly.

What State Law Does Without a Prenuptial Agreement

Part of the reason this conversation can feel abstract is that most people aren't clear on what actually happens without a prenup.

Without an agreement, state law controls how assets and debts are treated in divorce. In general terms, the law will determine what is considered marital property, what qualifies as separate property, and how things may be divided.

That sounds clean. In practice, it rarely is.

Assets owned before marriage may start as separate property but that doesn't always mean they stay entirely separate. How accounts are titled, whether assets get commingled, whether a spouse contributed to growth or maintenance, and how money moved during the marriage can all complicate the picture. A family home, business interests, inherited assets, and investment accounts can each carry their own nuances.

The same is true for debt, income earned during marriage, and appreciation on separate assets.

A useful place to start:

What would happen if we did nothing?

And then: Are we comfortable with that result, or do we want to define something different?

For some couples, the default rules may already feel reasonably fair. For others, particularly when there's family wealth, equity compensation, a business, or a meaningful difference in what each person is bringing in, state law may not reflect their actual situation very well.

A prenuptial agreement allows couples to be intentional about this. It gives them the ability to look at the default rules, identify where they agree, and decide where they want something different.

Where a Financial Planner and a Neutral Third Party Can Help

At some point, the conversation moves beyond whether to have a prenuptial agreement and into what it should actually address.

This is where things become more nuanced.

Many couples aren't struggling because they lack goodwill. They're struggling because they're trying to work through emotionally loaded topics without a clear framework. One person may be focused on protecting what they built before the relationship. The other may be thinking about fairness over the course of a future marriage. Both may be completely reasonable. They may simply be working from different definitions of security, fairness, and partnership.

This is one reason a neutral third party can make a real difference.

Financial planning creates a more structured way to work through these conversations before legal drafting begins. Instead of arguing in general terms, couples can slow down and get specific about what they each want, what they're trying to protect, and what a fair outcome would look like under different scenarios.

In practice, that often means working through questions like:

What assets are already separate, and how should they be treated going forward?

Will future earnings remain shared, or are there circumstances where separate treatment makes sense?

How should equity compensation, business ownership, or family money be handled?

If one partner steps back from work for family responsibilities, how should that be reflected?

What feels fair if the marriage lasts two years versus twenty?

Are there certain assets or future inheritances both partners already agree should remain separate?

This kind of conversation can help couples get genuinely aligned before attorneys begin turning ideas into legal language. It can also reveal where there's already agreement and where there are still meaningful differences to work through.

From there, an attorney drafts the agreement itself. And this part matters: each person should have their own attorney review the agreement before signing. A prenuptial agreement is a legal contract with long-term consequences. Independent legal review gives both parties a clear understanding of what they're agreeing to and more confidence in the outcome.

That doesn't make the process adversarial. In many cases, it does the opposite.

A Prenup Connects to Your Broader Financial Plan

A prenuptial agreement isn't a stand-alone legal task. It's part of a broader set of financial decisions that shape how a couple will operate together over time.

It connects directly to practical questions like:

How accounts will be titled

Whether certain assets should remain separate

How cash flow and investment accounts will be managed

What happens with future bonuses, equity compensation, or business growth

How each partner wants to approach long-term goals, family support, and major life transitions

It also has a way of surfacing issues that were already present, but unspoken. A disagreement about the document may actually be a disagreement about something bigger such as autonomy, security, fairness, or how the relationship will function financially over the long term.

Working through these questions within a broader planning context can help couples sort out what's legal, what's financial, and what's relational. Those categories overlap. They're not identical. A good process helps separate them enough to think clearly.

Final Thoughts

For most couples, the hardest part of this conversation is starting it.

Once it begins, it tends to lead somewhere useful. A clearer picture of how each person thinks about money, decisions, and what a fair shared life actually looks like.

That clarity has value well beyond whatever agreement you end up with.

If you're working through how to approach this and want help structuring the financial side in a grounded, practical way, that's exactly the kind of work we do with clients.

Frequently Asked Questions About Prenuptial Agreements

These are some of the questions that tend to come up most often as couples work through how to talk about a prenup and think through what it means for their relationship and finances.

-

The conversation typically happens during engagement or earlier if financial differences are already clear. Ideally, there is already a baseline understanding of each person’s finances before discussing a prenup.

-

Asking for a prenuptial agreement is not a red flag, it's often a sign of financial maturity. For women with established assets, equity compensation, or a business, it reflects a desire for clarity that protects both people. How the conversation is handled tends to matter far more than the request itself.

-

A financial advisor can help organize financial information, model potential outcomes, and provide context for how different decisions may impact each person financially.

-

Yes. A prenuptial agreement can address how future earnings, bonuses, RSUs, stock options, and business growth are treated during and after the marriage. Without one, state law determines how those assets are classified, which may not reflect your actual intentions.

-

Without a prenup, state law controls how assets are divided. Depending on your state, assets you owned before marriage, investment accounts, and equity compensation may be treated as marital property especially if finances became commingled over time. A prenuptial agreement lets you define a different structure.