Tax Planning for High Earners: What Actually Moves the Needle

Key Takeaways

The biggest tax opportunities are tied to decisions you're already making, not obscure loopholes. How you save, invest, handle equity comp, and time your income does far more than any exotic strategy.

Equity compensation is the most expensive blind spot we see, and 2026 made AMT sharper. ISO exercises can trigger the alternative minimum tax, and this year's lower phase-out thresholds ($500K single / $1M joint) pull more high earners into it. Timing matters enormously.

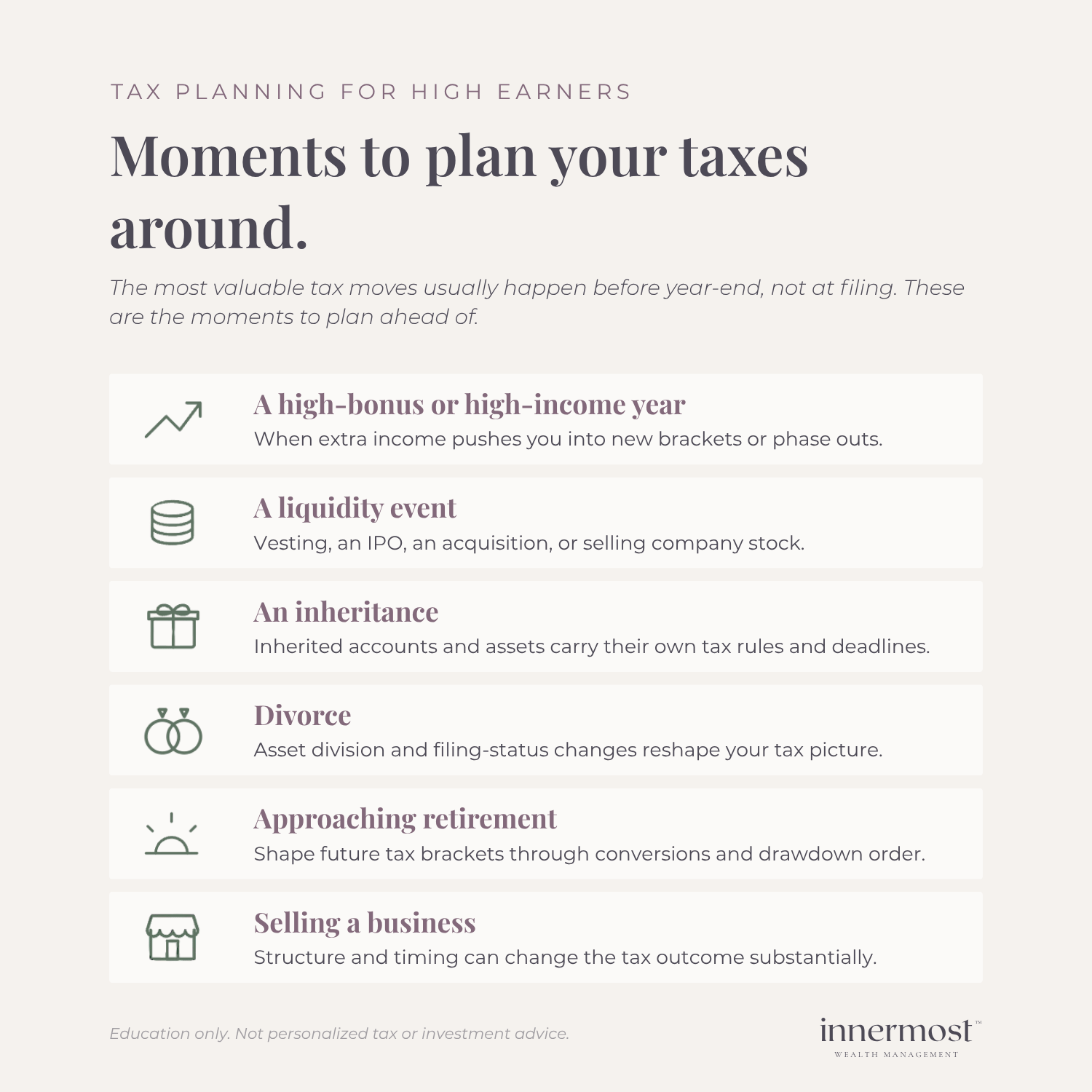

Tax planning has to be proactive. By the time you're at your CPA's desk in March, most of the valuable windows for the prior year have already closed. The decisions that lower your bill happen during the year.

There's a specific frustration that comes with earning more than you ever expected to and still feeling like you're not quite on top of it. You're saving. You're investing. By any measure you're doing well. And there's still a nagging sense that your April tax bill is bigger than it needs to be, and that someone who understood your situation could find things you're not seeing.

For most of the high-earning women we work with, that sense is right. Not because they've been careless. Because tax planning for high earners works differently than the general advice assumes, and at this income level the decisions that matter most are genuinely more complicated than "max your 401(k) and don't forget to file."

Here's the good news, and the thing we want you to take from this whole article: the biggest opportunities are almost never obscure. They're tied to decisions you're already making. How you save, how you invest, how you handle equity compensation, when you recognize income, and how you give. That's where the real money is. Not in some exotic strategy your neighbor's cousin swears by.

Let's walk through the moves that can make a difference, with the actual 2026 numbers, so you can see where you might be leaving money on the table.

Start with the accounts you already have.

Before anything clever, we want the basic accounts fully optimized, because they're often where the biggest, most reliable savings live. Less exciting to talk about. More effective than almost anything else.

Your 401(k) is the first lever. For 2026 you can defer up to $24,500 as an employee, and if you're 50 or older you can add an $8,000 catch-up on top of that. One 2026 change worth knowing if you're a high earner over 50: under the SECURE 2.0 rules, if you earned more than $150,000 in wages from your employer last year, your catch-up contributions now have to go in as Roth (after-tax) rather than pre-tax. That's not a loss, but it changes the tax math for the year, and it can catch people off guard.

For dual-income households, the common mistake isn't failing to contribute. It's contributing on autopilot. A lot of high earners default to maxing pre-tax and never revisit whether some of that money should be going to Roth instead. When you're projecting your tax picture out 20 or 30 years, having both pre-tax and Roth money gives you options later that you can't create after the fact. That balance is worth revisiting as your income and bracket change, not setting once and forgetting.

If your employer offers deferred compensation or you're a business owner, there's another layer. Deferred comp can smooth income into lower-earning years, and a well-designed business retirement plan can open up far more contribution room than a standard 401(k). Both are worth a real look rather than a passing glance.

The backdoor Roth: how it works when you earn too much.

Here's one that trips people up, because the rule sounds like a wall and it's really a door.

In 2026, you can't contribute directly to a Roth IRA once your income climbs past the phase-out range: $153,000 to $168,000 for single filers, and $242,000 to $252,000 for married couples filing jointly. Above those numbers, the front door is closed.

The backdoor Roth is the side entrance, and it's completely legitimate. You contribute to a traditional IRA (which has no income limit), then convert that money to a Roth. The result is the same tax-free growth you'd have gotten from a direct Roth contribution, just reached by a different route. Done consistently over years, it builds a meaningful pool of money that grows and comes out tax-free in retirement, which becomes more valuable the longer your time horizon.

One real caution, because this is where people get a surprise tax bill: the pro-rata rule. If you already have pre-tax money sitting in traditional IRAs, the IRS won't let you cherry-pick only the after-tax dollars to convert. It treats your conversion as a proportional mix of pre-tax and after-tax money, and you owe tax on the pre-tax portion. If you have an old rollover IRA from a previous job, that can turn a clean backdoor Roth into an expensive one. There are ways around it, like rolling that pre-tax money into your current employer's 401(k) first, but you want to sort that out before you convert, not after.

The HSA is the most underused tax break high earners have.

Most people treat a Health Savings Account like a checking account for medical bills. Money in, money out, done. For a high earner, that's leaving one of the best deals in the tax code on the table.

An HSA is the only account that's tax-advantaged three separate times. Your contributions are deductible, the money grows tax-free, and withdrawals for qualified medical expenses are tax-free too. Nothing else does all three. For 2026, if you have a qualifying high-deductible health plan, you can contribute $4,400 as an individual or $8,750 for family coverage, plus another $1,000 if you're 55 or older.

Here's the move most people miss. Instead of spending the HSA on this year's copays, pay those out of pocket, leave the HSA invested, and let it grow for decades. Save your medical receipts along the way. You can reimburse yourself for those expenses at any point in the future, even years later, which means you've effectively created a stealth retirement account that came with a tax deduction on the way in. For a high earner who can afford to cover current medical costs from cash flow, this becomes one of the most efficient accounts you own.

Equity compensation: where the most expensive tax mistakes happen.

This is the section I want to spend the most time on, because it's where we see the costliest mistakes, and where women in particular tend to underestimate what they've actually built. I've heard "it's not really that much" more times than I can count. Then we pull up the numbers together, and it is. It really is.

RSUs, ISOs, ESPPs, stock options, restricted shares. These create real complexity: withholding shortfalls, concentrated stock risk, exercise timing, blackout windows, and one that's biting harder in 2026, the alternative minimum tax.

Let me explain AMT plainly, because it's the one that surprises people. AMT is a parallel tax system with its own rules. You calculate your taxes the normal way, then calculate them again under AMT rules, and pay whichever is higher. When you exercise incentive stock options (ISOs) and hold the shares, the "paper gain" between your strike price and the stock's value gets counted as income under AMT, even though you haven't sold anything or received a dollar. That's how people get a tax bill for money they never touched.

Here's why this matters more in 2026. A recent tax law change lowered the income levels where the AMT exemption starts to disappear, down to $500,000 for single filers and $1 million for married couples filing jointly, and it made that exemption phase out twice as fast as before. The exemption itself is $90,100 for single filers and $140,200 for joint filers in 2026. In plain terms: AMT is reaching into income ranges it left alone for years, so more people exercising options are going to run into it. If you have ISOs and you're anywhere near those income levels, the timing of when you exercise can change your tax bill by a lot. Spreading exercises across multiple years instead of all at once is often the difference. This is worth modeling before you click the button, not after.

The other equity-comp trap is emotional, and it's expensive in a different way. We've watched clients hold huge concentrated positions in their employer's stock far longer than they wanted to, not because they believed in the company, but because selling would trigger taxes. Those positions become golden handcuffs. They know they should diversify, they understand the risk, and taxes keep them frozen. Sometimes paying the tax today is what buys you a diversified, lower-risk financial life tomorrow. That tradeoff deserves careful thought with someone who can see your whole picture. We walked through exactly this kind of vesting-event decision with Emily, a tech professional navigating equity compensation, and it's a good example of what the process looks like in practice.

Tax-efficient investing: the part that happens after the paycheck.

Taxes don't stop once your income lands in your account. How your portfolio is built matters too, and at higher income levels the stakes on each decision are bigger.

A few things can make a difference here. Tax-loss harvesting means selling an investment that's down to capture the loss for tax purposes, then reinvesting in something similar so you stay in the market. Asset location means putting your least tax-efficient investments (like bonds or actively managed funds) inside tax-sheltered accounts, and keeping the tax-efficient ones in your taxable account. Same investments, better placement, lower lifetime tax.

The most common quiet drain we see is actively managed mutual funds sitting in a taxable account. Many of those funds pass through taxable capital gains every year whether or not you sold anything, which creates a tax drag you never chose. The fix is often straightforward once you can see it. This is part of why we think about investment management and tax planning together rather than separately, because a portfolio decision is almost always a tax decision too.

Charitable giving that lowers your taxes, not just your guilt.

If giving is already part of your life, the way you structure it can do a lot more tax work than writing checks.

Three moves worth knowing. Donating appreciated stock directly, instead of selling it and giving cash, lets you skip the capital gains tax entirely and still deduct the full value. A donor-advised fund lets you make a large contribution in one high-income year, take the deduction now, and then distribute the money to charities over time. And "bunching," where you combine two or three years of giving into a single year, can push you above the standard deduction threshold in that year so your giving actually counts.

These matter most in your biggest income years: a large vesting event, a major bonus, a business sale, a liquidity event. Those are exactly the moments charitable planning does the most work, and exactly the moments the window closes fastest if nobody's watching the calendar.

Roth conversions: powerful in the right year, wrong in most.

A Roth conversion means moving money from a pre-tax account into a Roth, paying the tax now so it grows tax-free forever after. The catch is that you pay that tax at your current rate, so doing it in a high-income year usually makes no sense.

Where conversions shine is the low-income window. A career transition, a sabbatical, maternity leave, the early years of retirement before Social Security and required withdrawals kick in, or a temporary dip in business income. In those years your rate is lower, so converting costs less, and you're locking in tax-free growth for decades. The best results come from planning conversions across several years rather than reacting to any single one. If you want the fuller picture of how these windows open in the years around leaving work, we get into it in the emotional and financial stages of retirement.

Strategies worth being skeptical of.

Not every tax strategy deserves your attention. Some deserve real suspicion.

Be cautious when someone is pushing a strategy mainly because it promises massive savings. Buying real estate purely for the write-offs. Financial products you don't fully understand. Business structures that add layers of complexity. Holding investments you don't actually want just for a tax benefit. We've seen people spend more chasing a strategy than they ever saved from it.

Here's a simple test: good tax planning reduces the complexity in your financial life. If a strategy needs a long explanation before you can understand why it helps you, that's a reason to slow down, not speed up.

Why waiting until tax season costs you.

The single most common thing we see: someone sits down with their CPA in March and asks what they could have done differently last year. The honest answer is usually "quite a bit," and most of those windows are already closed.

Almost everything in this article is a decision made during the year, not at filing time. The Roth conversion in your low-income year. The ISO exercise timing. The charitable gift in your big bonus year. By April, those doors have shut. Waiting until tax season to think about taxes means spending your energy looking backward at a year you can no longer change.

This is also why we coordinate directly with our clients' CPAs. A financial planner and a CPA looking at the same picture at the same time catches things that neither catches alone. Your CPA is often focused on filing an accurate return for the year that just ended. Proactive tax planning is about shaping the year that's still in front of you. You want both. If you want to see how that ongoing, year-round approach fits into a full plan, that's the heart of our comprehensive financial planning work.

A quick self-check: are you leaving money on the table?

You don't need a full plan to spot the gaps. Run through these. If you answer "not sure" or "no" to several, there's likely real money being left behind:

Are you contributing to both pre-tax and Roth, or defaulting entirely to one?

If your income is over the Roth limit, are you using a backdoor Roth (and have you checked the pro-rata rule)?

Are you investing your HSA for the long term, or spending it on current bills?

If you have equity comp, do you know whether your ISO exercises could trigger AMT this year?

Are your least tax-efficient investments tucked inside tax-sheltered accounts?

In your highest-income years, are you giving appreciated stock instead of cash?

Are you saving Roth conversions for your lowest-income years?

Is your financial planner talking to your CPA, or are they working in separate silos?

If a few of those landed, you're not behind, and nothing here is a personal failing. It just means your tax approach hasn't caught up to your income yet, which is one of the most common and most fixable situations we see. If you'd like a second set of eyes on where the opportunities are in your specific picture, that's exactly the kind of thing we do together.

Where this all connects.

Taxes don't live in their own box. They touch your investments, your retirement timeline, your equity comp, your giving, and every major life transition. A decision in one area moves the others, which is why looking at them together beats optimizing each one alone.

Building real wealth should create more freedom, not a second job you didn't apply for. Tax planning for high earners isn't about hunting down every possible deduction. It's about making sure the decisions you're already making are structured as well as they can be, so you're not leaving meaningful money behind while you're busy running the rest of your life.

Frequently asked questions about tax planning for high earners.

-

Tax planning for high earners is the proactive structuring of income, investments, and equity compensation to reduce taxes at levels where the rules get more complex. It differs from general tax advice because it addresses issues most guidance skips: Roth phase-outs, the alternative minimum tax on stock options, concentrated stock, and multi-year income timing. The focus is on structuring the big decisions you're already making, not hunting individual deductions.

-

High earners should plan taxes proactively throughout the year, not at filing time. Most tax-saving moves, including Roth conversions, equity compensation timing, and charitable giving, have to happen during the tax year itself, because by the time you file in spring, the windows for the prior year have already closed. Planning ahead of bonuses, vesting, and liquidity events is where the real savings come from.

-

Equity compensation creates some of the largest tax consequences high earners face. RSUs are taxed as ordinary income when they vest, ISOs can trigger the alternative minimum tax when you exercise and hold, and concentrated employer stock carries both risk and a tax cost to unwind. In 2026, lower AMT phase-out thresholds ($500,000 single, $1 million joint) mean ISO exercises trigger AMT more easily, so spreading exercises across years often lowers the bill.

-

You benefit most from both, working together. A CPA typically focuses on accurately filing your return for the year that just ended, while a financial planner proactively shapes the decisions in the year ahead. Coordination between them catches opportunities neither sees alone. A fee-only planner has no product to sell, so the advice centers on your situation rather than a commission.

-

High-earning women should prioritize the high-impact basics first: maximizing and diversifying retirement contributions between pre-tax and Roth, investing an HSA for the long term instead of spending it, and getting equity compensation timing right. Equity compensation is where we most often see women underestimate what they've built and face the largest avoidable tax bills. Charitable structuring and multi-year Roth conversions add value after those.

This article is general in nature and is not tax advice. Tax rules change and every situation is different. The 2026 figures cited reflect IRS inflation adjustments for the 2026 tax year. We recommend working with both a financial planner and a CPA to decide what makes sense for you.