Retirement Taxes in Michigan: What Nobody Tells You Until It's Too Late

Catching the evening light along the Lake Michigan shoreline. Shot by Kimberly during a summer camping trip at Nordhouse Dunes, just outside of Ludington and Manistee.

Key Takeaways

Beginning with the 2026 tax year, Michigan's retirement income phase-in is complete. Eligible taxpayers may qualify for the full retirement and pension deduction available under current law, subject to applicable limits and eligibility requirements.

Michigan doesn't tax Social Security benefits, but federal taxes, required minimum distributions (RMDs), capital gains, Medicare premium surcharges (IRMAA), and other income sources can still have a significant impact on your overall retirement tax bill.

Retirement tax planning is most effective when financial decisions are evaluated together rather than individually. The timing of withdrawals, Roth conversions, Social Security, investment sales, and other major income events can affect your lifetime tax liability.

Most people spend decades preparing for retirement. They contribute to retirement accounts, build investment portfolios, accumulate company stock, grow businesses, and save consistently throughout their careers.

As retirement approaches, the questions begin to change. Instead of focusing on how to build and accumulate wealth, the focus shifts to how and when to best use it.

Which accounts do I pull from first?

What happens when required minimum distributions kick in?

Should I be doing Roth conversions?

When do I sell concentrated stock positions?

How much of this will Michigan tax?

Why is my tax bill still this high?

In my experience, many people expect their taxes to decline once they stop working. What often surprises them is that retirement changes where taxable income comes from, not necessarily how much tax planning is required.

Traditional retirement accounts, appreciated brokerage investments, employer stock, real estate, and business interests can all continue to create tax consequences after you retire. Decisions about when to withdraw money, sell investments, claim Social Security, or complete a Roth conversion can all affect your overall tax picture.

Michigan's retirement tax rules create planning opportunities, but they're only one part of the picture. Federal taxes, required minimum distributions, investment income, Medicare premiums, and the timing of major financial decisions all influence how much you may pay over the course of retirement.

In this article, we'll discuss how retirement income is taxed in Michigan, where federal tax rules continue to affect retirees, and the key planning considerations that can help you make more informed financial decisions throughout retirement.

Does Michigan tax social security benefits?

Michigan does not tax Social Security benefits, which is one reason the state is often considered relatively retirement-friendly.

At the federal level, however, Social Security benefits may be subject to federal income tax depending on your overall income. Traditional IRA and 401(k) withdrawals, pension income, investment income, capital gains, rental income, and other taxable income can all affect how much of your Social Security benefits become taxable.

Because of that, deciding when to claim Social Security shouldn't be viewed as a standalone decision. Coordinating Social Security with retirement account withdrawals, investment income, and other sources of income can help you better manage your overall tax picture throughout retirement.

Michigan retirement and pension income tax rules.

Under the Lowering MI Costs Act (Public Act 4 of 2023), Michigan spent four years gradually restoring retirement income exemptions that were cut back in 2011. That phase-in is now complete. Beginning with the 2026 tax year, the birth-year tier system (Tier 1, Tier 2, and Tier 3) is fully phased out, and eligible retirees may qualify for Michigan's full retirement and pension deduction, subject to applicable limits and eligibility rules.

For 2026, the maximum deduction is $67,610 for single filers and $135,220 for married couples filing jointly. Military pensions remain fully exempt without a dollar limit, and certain public safety retirees (including police officers, firefighters, and corrections officers) may qualify for an unlimited deduction on eligible public pension income.

Public Act 24 of 2025 added another change worth knowing about. Michigan taxpayers born after 1952 and aged 67 or older can now claim both the standard deduction and the Social Security deduction simultaneously for tax years 2026 through 2028. Previously, qualifying retirees had to reduce their standard deduction by the amount of their Social Security deduction. That limitation has been temporarily eliminated, although the standard deduction is still reduced by the personal exemption amount.

Even with Michigan's expanded retirement tax deductions, federal taxes, investment income, required minimum distributions, and withdrawal sequencing continue to create significant planning complexity and opportunity.

Michigan's four-year phase-in is finished. Starting in 2026, the old birth-year tiers are gone and eligible retirees get one full retirement and pension deduction.

Taxation of traditional retirement account withdrawals.

For many years, maximizing pre-tax retirement accounts was sound advice. Contributing to a traditional 401(k) or IRA reduced taxable income during your highest-earning years and allowed investments to grow tax-deferred. For many people, it was exactly the right strategy.

It's also important to remember that many of today's retirees spent much of their careers without a Roth 401(k) option. Roth 401(k)s first became available in 2006, when many people who are now retired or approaching retirement were already well into their careers. Even after that, employer adoption took time, and many retirement plans continued to offer only traditional pre-tax contributions. As a result, it's common for people approaching retirement to have most, or even all, of their retirement savings in tax-deferred accounts.

Because the tax deduction is received today and the tax bill may not come for decades, many people don't spend much time thinking about what those withdrawals will eventually look like. That's understandable. During your working years, the focus is usually on saving as much as possible, not on how you'll withdraw that money 20 or 30 years later.

By retirement, it's easy to think of a traditional 401(k) or IRA as one large pot of money. In reality, part of that balance represents future taxes. A $1 million traditional 401(k) isn't the same as having $1 million available to spend. The amount you ultimately keep depends on how and when you withdraw the money and what other taxable income you have in retirement.

That's where planning becomes important. If a large portion of your wealth is held in traditional IRAs, 401(k)s, and rollover accounts, your flexibility in retirement may be more limited than you expect. Withdrawals from these accounts are generally taxed as ordinary income, and required minimum distributions eventually require you to take money out whether you need the income or not. When those distributions are combined with Social Security, pension income, investment income, or other taxable income, the overall tax impact can be greater than you expect.

Having assets across taxable, tax-deferred, and Roth accounts can provide more flexibility when deciding where retirement income comes from each year. If most of your savings are currently in pre-tax accounts, it's worth understanding how that could affect your retirement income strategy and discussing your options with a qualified financial or tax professional before you retire.

Roth accounts & tax-free income in Michigan.

Qualified withdrawals from Roth IRAs and Roth 401(k)s are generally tax-free for both federal and Michigan income tax purposes. That can make Roth assets a valuable source of retirement income because qualified withdrawals generally don't increase your taxable income.

Some retirees also evaluate Roth conversions, which involve moving money from a traditional retirement account into a Roth account. The amount converted is generally taxable for both federal and Michigan tax purposes in the year of the conversion, but future qualified withdrawals may be tax-free.

Whether a Roth conversion makes sense depends on your income, expected future tax rate, and overall retirement plan. Lower-income years, such as the period after retirement but before claiming Social Security or before required minimum distributions begin, can sometimes provide an opportunity to evaluate whether a conversion is appropriate.

I converted part of my own traditional IRA during the first year I was building Innermost Wealth Management. My income was lower than it had been previously, so I estimated the tax impact, set aside cash to pay both federal and Michigan taxes, and completed the conversion. Given my circumstances, I believed it was an appropriate time to convert. Every situation is different, which is why Roth conversions should be evaluated as part of an overall retirement tax strategy.

Michigan tax on investment income.

Taxable brokerage accounts can be an important source of retirement income because they generally provide more flexibility than traditional retirement accounts. Unlike traditional IRAs and many employer retirement plans, brokerage accounts aren't subject to required minimum distributions, age-based withdrawal rules, or many of the restrictions that apply to tax-advantaged retirement accounts. That gives you more control over when you access your money, sell investments, and recognize taxable income.

At the Michigan level, investment income is generally taxed at the state's flat 4.25% individual income tax rate. That includes interest, dividends, and capital gains. Michigan does not provide a separate preferential tax rate for long-term capital gains like the federal government does. Residents born before 1946 may be eligible for an investment income subtraction, although the annual limit is reduced by any retirement benefit subtraction claimed that year.

Federal tax treatment is more complex. Depending on your income and the type of investment sold, capital gains may affect not only your federal tax bill, but also net investment income tax exposure, Medicare premiums through IRMAA, and the portion of your Social Security benefits that is taxable.

This becomes especially important if you own concentrated company stock, highly appreciated investments, inherited assets, real estate, or business interests. Deciding when to sell those assets can affect more than just the taxes you owe in the current year. It can influence your broader retirement income strategy as well.

Where your retirement income comes from each year changes what you owe. Holding assets across all three account types gives you more control over your tax bill.

Michigan property taxes and retirement planning.

Property taxes are often overlooked in retirement planning. Conversations focus on retirement accounts, investment income, and Social Security, while housing decisions are viewed primarily as lifestyle choices.

In reality, where you live can have a meaningful impact on your long-term retirement expenses. Even if you've paid off your mortgage, property taxes remain an ongoing cost and impact your retirement cash flow.

Michigan property tax rates vary significantly by location. Local millage rates, taxable values, principal residence exemptions, and whether a property qualifies as a primary residence or second home can all affect your annual property tax bill. Two homes with similar purchase prices can have very different annual property taxes depending on where they're located.

If you're considering downsizing, relocating, or purchasing a second home, it's important to evaluate property taxes alongside the purchase price, maintenance costs, homeowners insurance, and your overall retirement budget. In some cases, a lower-cost home may have higher ongoing ownership costs than expected, while a more expensive home may have lower annual property taxes.

Property taxes are only one piece of the decision, but understanding how they'll affect your long-term cash flow can help you make a more informed choice before you buy or move.

What is IRMAA and how does it affect retirement income?

IRMAA (Income-Related Monthly Adjustment Amount) is a federal surcharge set by the Centers for Medicare & Medicaid Services. It applies equally in Michigan and everywhere else. When your Modified Adjusted Gross Income crosses certain thresholds, your premiums go up for both parts of Medicare that carry premiums.

Part B - covers doctor visits, outpatient care, lab work, and medical equipment

Part D - covers prescription drugs

Because Medicare premiums and IRMAA income thresholds are adjusted periodically, the figures below apply to the 2026 coverage year and should be verified against current CMS guidance when planning.

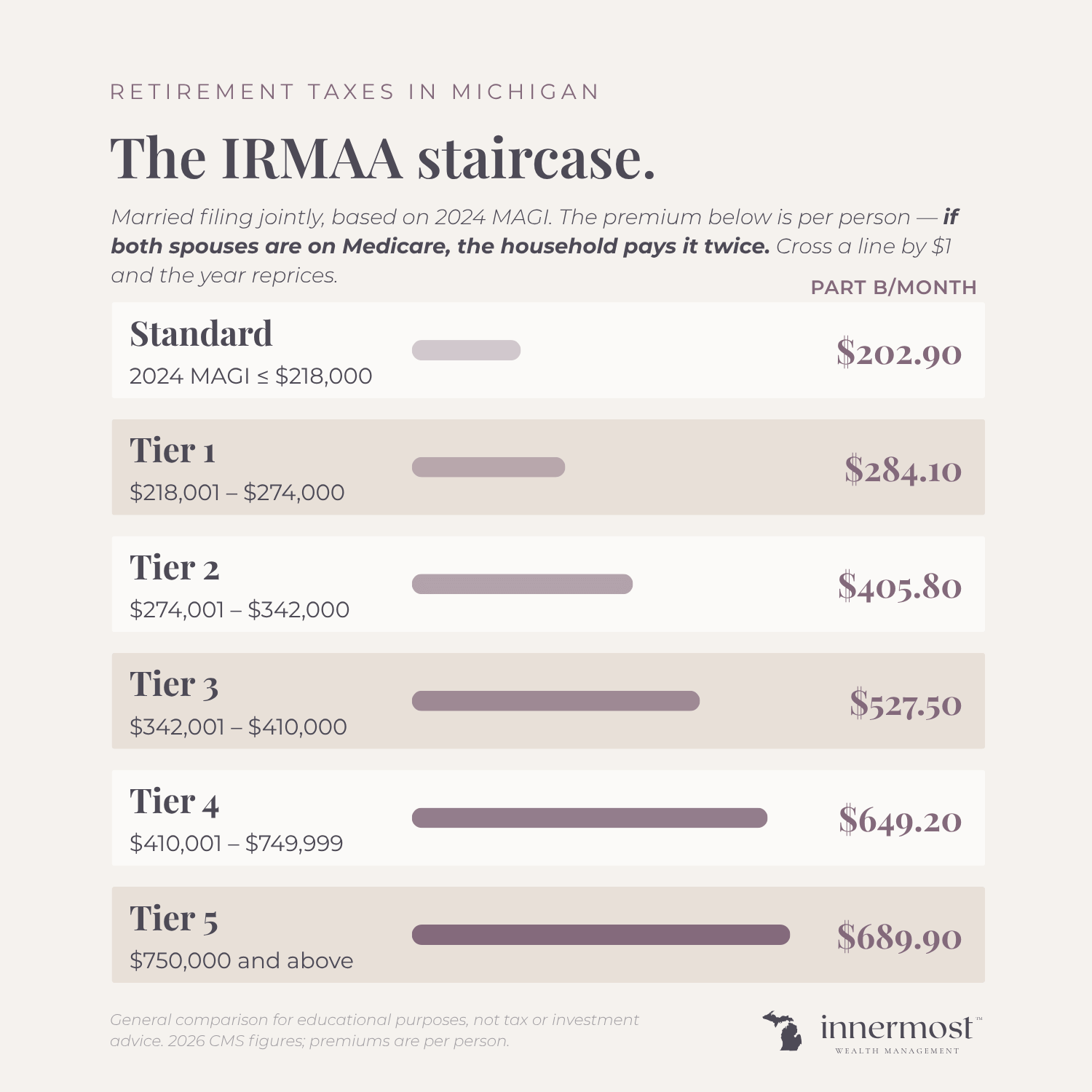

For Medicare coverage in 2026, IRMAA is generally based on your 2024 modified adjusted gross income (MAGI). That two-year lookback is the part that catches people off guard: a large income event in 2024 affects Medicare costs in 2026, not immediately. For single filers with 2024 MAGI of $109,000 or less (married filing jointly at $218,000 or less), the standard Part B premium is $202.90 per month with no Part D surcharge. At the highest tier, single filers with MAGI over $500,000 pay $689.90 per month for Part B plus $91.00 monthly for Part D.

The cliff effect is what makes this genuinely dangerous in planning. One dollar over a bracket threshold moves you into the next IRMAA tier. A Roth conversion that pushes MAGI $5,000 over a cutoff can add thousands of dollars in Medicare costs for the year, not because the conversion was wrong, but because nobody modeled the Medicare impact before pulling the trigger. For a married couple, crossing from Tier 1 to Tier 2 alone costs an additional $3,475 per year in Medicare premiums. That recurs every year your income stays above the line.

If you experienced a qualifying life event (retirement, divorce, death of a spouse), you can appeal your IRMAA determination using Form SSA-44 with the Social Security Administration. That option exists, it works, and most people have never heard of it.

Something that almost never gets planned for: what happens to Medicare costs when a spouse dies. When a surviving spouse files as Single, the IRMAA brackets are roughly half the married filing jointly thresholds. A couple comfortably in Tier 1 as joint filers can land two tiers higher as a single filer with no actual change in income. For a surviving spouse, who is statistically more likely to be a woman, that's thousands of dollars more per year in Medicare costs at exactly the moment when financial life is already hard. Planning for this scenario before it happens is worth the conversation. One effective strategy is building Roth assets while both spouses are alive, so the surviving spouse has tax-free income that doesn't push Medicare costs higher.

One more thing: qualified Roth IRA distributions don't count toward MAGI for IRMAA purposes. Traditional IRA distributions do. Building Roth assets before retirement can help reduce the cost of Medicare.

For single filers, the total Medicare Part B premium climbs with income. Cross a bracket line by even one dollar and the whole year reprices to the higher tier.

For married couples, the premium shown is per person — if both spouses are on Medicare, the household pays it twice. One dollar over a line reprices the year for both.

How major income events affect retirement taxes.

Large tax bills in retirement are often the result of several major financial decisions happening in the same year.

For example, someone might sell a business, sell real estate, take a large IRA withdrawal, complete a Roth conversion, sell a concentrated stock position, and begin claiming Social Security within a relatively short period. Each decision may make sense on its own, but together they can significantly increase taxable income for the year.

Coordinating those decisions over multiple tax years can help manage the overall tax impact. In some situations, it may make sense to spread income over several years, adjust the timing of withdrawals, or postpone certain transactions.

The order in which you withdraw money from taxable brokerage accounts, traditional retirement accounts, and Roth accounts also affects your tax picture. The best approach depends on your income sources, projected required minimum distributions, Social Security timing, and your overall financial goals.

The emotional side of retirement tax planning.

One aspect of retirement that often receives less attention is the emotional adjustment.

For decades, the focus has been on saving, investing, delaying gratification, and preparing for the future. Those habits are rewarded throughout your working years. Retirement asks something different. Instead of accumulating wealth, you're expected to begin using it.

For some people, that transition feels natural. For others, it can be surprisingly difficult, even when the numbers clearly show they can afford to retire. I've worked with people who had more than enough to support the lifestyle they wanted but still felt guilty about spending money, worried about running out, or continued treating every purchase as though they were still in their peak earning years.

I see this especially with women who have spent decades managing households, raising families, building careers or businesses, and putting other people's needs ahead of their own. They often become very comfortable making financial decisions for everyone else, but much less comfortable making decisions that benefit themselves.

That's one reason I believe retirement planning should account for more than taxes, investments, and withdrawal strategies. A financial plan should also give you the confidence to use your wealth in a way that reflects the life you've spent decades working toward.

If this part of retirement resonates with you, I wrote more about the emotional transition into retirement here.

Retirement tax planning in a nutshell.

Retirement tax planning is the process of making informed decisions about when and how you recognize income throughout retirement. That includes decisions about retirement account withdrawals, Social Security, investment sales, Roth conversions, healthcare costs, charitable giving, and other financial events that can affect your tax bill.

No single strategy works for everyone. The right approach depends on your income sources, assets, goals, and the tax rules that apply to your situation. Michigan's retirement tax rules can create valuable planning opportunities, but they're only one piece of a much larger picture.

If you're approaching retirement or are already retired and would like help building a tax-efficient retirement income strategy, I'd be happy to help. You can schedule an initial consultation here.

Frequently asked questions about retirement taxes in Michigan.

-

Starting with the 2026 tax year, Michigan completed its four-year phase-in under the Lowering MI Costs Act (Public Act 4 of 2023). All eligible Michigan retirees can now deduct 100% of their combined public and private retirement and pension income from state taxes regardless of birth year. The 2026 exemption caps are $67,610 for single filers and $135,220 for married filing jointly. Military pensions remain fully exempt with no cap. Public safety retirees including police, firefighters, and corrections officers can claim an unlimited exemption on public pension income.

-

No. Michigan does not tax Social Security benefits at the state level. However, depending on your total income, up to 85% of your Social Security benefits can still become taxable at the federal level. IRA withdrawals, pension income, capital gains, and investment income all feed into that federal calculation, which is why Social Security timing decisions have to be evaluated alongside the rest of your retirement income picture, not in isolation.

-

IRMAA stands for Income-Related Monthly Adjustment Amount, a federal Medicare surcharge that applies when your Modified Adjusted Gross Income exceeds certain thresholds. For 2026, the surcharge kicks in at $109,000 MAGI for single filers and $218,000 for married couples filing jointly, based on your 2024 tax return. The surcharges apply equally in Michigan and every other state. Earning even $1 over a bracket threshold triggers the full surcharge for that tier, which can add thousands of dollars per year to Medicare costs. Roth conversions, business sales, and large IRA distributions are the most common triggers.

-

For many Michigan retirees, Roth conversions during lower-income years including career transitions, early retirement before Social Security starts, or temporary income dips may create long-term tax and Medicare savings. Qualified Roth distributions don't count toward MAGI for IRMAA purposes, which means building Roth assets reduces both future tax exposure and Medicare premium costs. The right conversion amount depends on your specific income sources, projected RMDs, IRMAA bracket position, and Social Security timing.

-

Michigan is more retirement-friendly than most people realize, and it's getting better. Starting in 2026, all eligible Michigan retirees can deduct 100% of qualifying retirement and pension income from state taxes regardless of birth year, up to $67,610 for single filers and $135,220 for married filing jointly. Michigan does not tax Social Security benefits, military pensions are fully exempt, and the state's flat income tax rate remains at 4.25% for 2026.

That said, favorable state tax treatment doesn't eliminate federal tax complexity. RMDs, capital gains, IRMAA, and withdrawal sequencing still require planning for anyone who has built significant wealth.

This article is for general informational and educational purposes only and does not constitute tax, legal, investment, or financial advice. Michigan tax laws are subject to change, and individual circumstances vary. Please consult a qualified CPA, tax professional, or other appropriate advisor regarding your specific situation.

Sources

Michigan Department of Treasury — Retirement and Pension Benefits https://www.michigan.gov/taxes/iit/tax-guidance/tax-situations/retirement-and-pension-benefits

Michigan Revenue Administrative Bulletin 2026-1 https://www.michigan.gov/taxes/rep-legal/rab/2026-revenue-administrative-bulletins/revenue-administrative-bulletin-2026-1

Michigan Public Act 24 of 2025 https://legislature.mi.gov/documents/2025-2026/publicact/htm/2025-PA-0024.htm

Michigan 2026 Income Tax Rate Confirmation — State Treasurer's Office https://content.govdelivery.com/attachments/MITREAS/2026/04/15/file_attachments/3619120/FY%202026%20Income%20Tax%20Rate%20Letter.pdf

CMS 2026 Medicare Parts A & B Premiums and Deductibles https://www.cms.gov